Subscription Rails: eGIRO, UPI AutoPay, SEPA SDD, Pix Automático

PayNow can't pull recurring. UPI AutoPay tripled in one year. Pix Automático launched June 2025. What each market's recurring billing rail delivers.

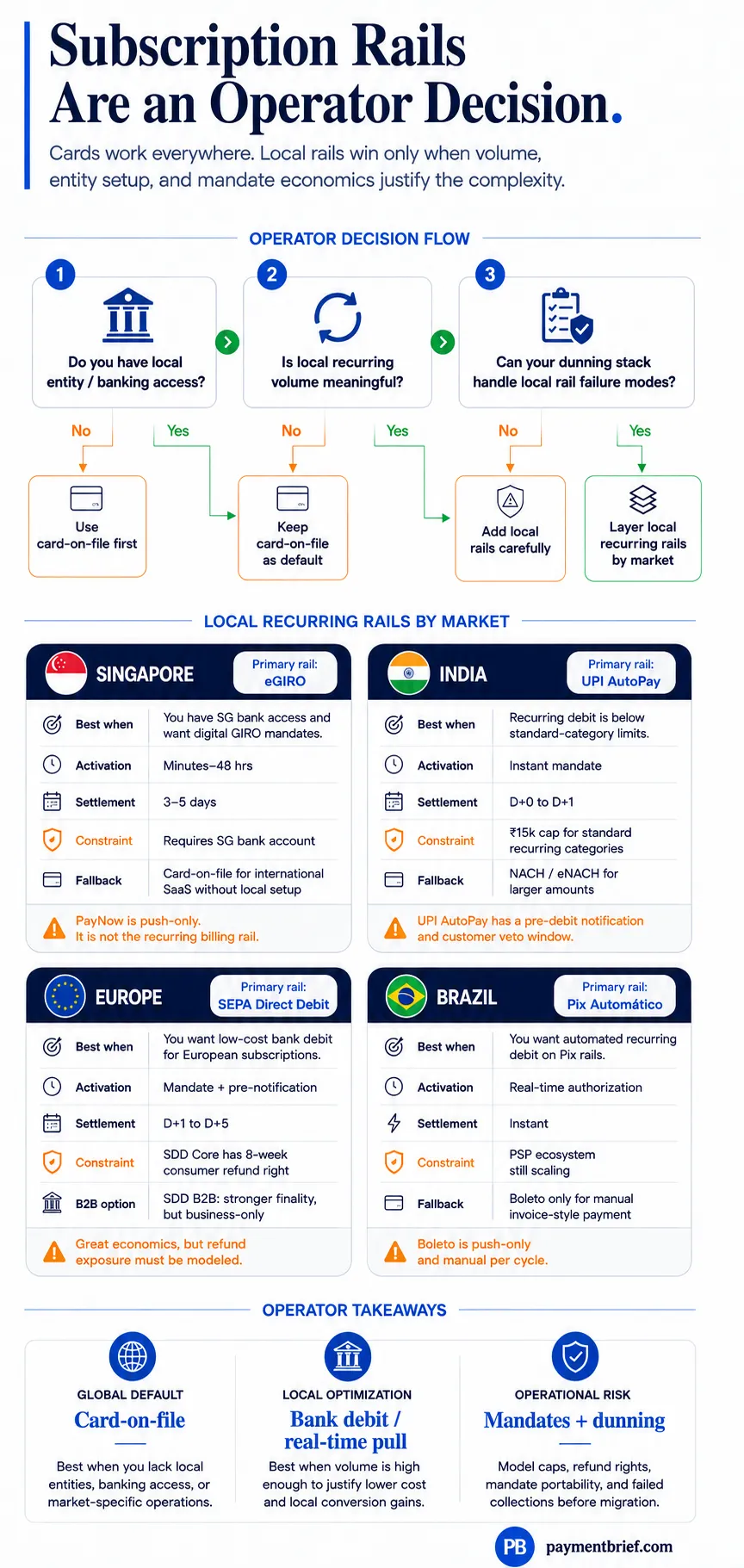

PayNow is push-only — eGIRO handles recurring billing in Singapore. UPI AutoPay hit 175M monthly transactions in Jan 2025, tripling YoY. SEPA SDD Core has an 8-week consumer refund right. Pix Automático launched June 2025. Cards remain default for operators without local entity.

PayNow does not support recurring or subscription payments — it is a push-only credit transfer. For recurring billing in Singapore, operators use eGIRO (digital bank debit mandate, minutes to activate). In India, UPI AutoPay is the bank-debit equivalent (₹15,000 cap for standard categories; 175M monthly transactions as of January 2025). In Europe, SEPA Direct Debit Core handles recurring with an 8-week no-questions-asked consumer refund window; B2B scheme removes this right. Brazil launched Pix Automático in June 2025 — a pull-debit layer on the Pix instant rail, instant settlement. Cross-border SaaS without local entity presence defaults to card-on-file: universal PSP support, card network updater services, and no banking relationship required.

The default subscription billing stack for a cross-border SaaS company is: Stripe for everything, card-on-file globally, recurring charges via merchant-initiated transactions. It works in every market. It requires no banking relationships. It benefits from Visa Account Updater and Mastercard ABU, which automatically push new card numbers when cards expire or get reissued — self-healing against the leading cause of involuntary churn.

It is also expensive in every market, has structurally higher failure rates than bank debit, and leaves significant recoverable revenue on the table in markets where real-time rails have built pull-payment capabilities.

The rails are maturing fast. UPI AutoPay tripled its monthly transaction volume in one year. Brazil launched Pix Automático in June 2025 — the first pull-debit layer on a real-time settlement rail. eGIRO compressed Singapore GIRO mandate setup from weeks to minutes. SEPA Direct Debit has been running reliably for years, SCA-exempt, at pennies per transaction.

This article covers what each rail actually delivers for recurring billing — and where it breaks down. For the high-level comparison of real-time rails across architecture and fees, the rail comparison piece covers nine rails at breadth. This goes deeper on the recurring-billing use case specifically.

The pull payment problem

One-time and recurring payments look similar from the outside — both move money from a payer to a merchant. The mechanics are completely different.

A one-time payment is initiated by the payer. They click, authenticate, and authorize. The money moves.

A recurring payment needs the merchant to initiate the collection — the payer has already given standing authorization. This "pull" mechanic requires the payer's bank to accept a debit instruction from an institution the payer has pre-authorized. Every market has a different answer to how that authorization is recorded, verified, and revoked.

Card networks solved this at global scale: cardholder stores card-on-file with the merchant, the MIT (merchant-initiated transaction) framework handles the recurring charge. The tradeoffs: card processing fees, card expiry and reissuance failures, and SCA friction in Europe for the initial authenticated setup.

Local bank-debit rails have structural advantages — lower per-transaction cost, no expiry problem, higher authorization rates on established mandates — but each requires market-specific infrastructure, entity presence, and operational setup.

Singapore: PayNow is not the answer

The most common operator misconception about Singapore payments is that PayNow supports recurring billing. It does not.

PayNow is a credit transfer overlay on FAST (Fast and Secure Transfers). It moves money from payer to payee — the payer initiates every single transaction. There is no pull mechanism, no mandate system, no way for a merchant to initiate a debit. For one-time payments — checkout, invoice settlement, B2B transfers — PayNow is excellent: instant, free for consumers, widely adopted across Singapore's banking network. For subscriptions, it is structurally the wrong instrument.

The actual recurring billing rail in Singapore is GIRO (Interbank GIRO), the direct debit scheme underlying utilities, insurance, CPF contributions, and a significant share of B2C subscription billing. Legacy GIRO's problem was setup friction: paper mandate forms, up to 21 working days to activate, requiring customers to mail physical documents. Effective for utilities with captive customer relationships; effectively unusable for SaaS with a checkout-to-billing flow.

eGIRO, launched in 2021 by MAS and the Association of Banks in Singapore (ABS), solved this. eGIRO is a digital mandate setup API: the customer authenticates directly with their bank, the mandate activates within minutes for individual accounts and under 48 hours for corporate accounts. Aspire, Razorpay SG, and others position it specifically for SaaS subscription collections. From July 2024, Prudential discontinued hardcopy GIRO applications for eGIRO-participating banks — the industry has moved.

The practical ceiling: eGIRO requires a Singapore bank account and eGIRO-participating bank coverage. Most international SaaS companies billing Singapore customers without a local entity still default to card-on-file — which does support PayNow for one-time checkout but uses card rails for subscriptions.

One development to track: MAS and ABS announced Singapore Payments Network (SPaN) in February 2025, incorporated June 2025, to consolidate governance of FAST, PayNow, GIRO, eGIRO, and SGQR under one entity. SPaN does not add pull capability to PayNow by itself — but the trajectory of markets like India (UPI → UPI AutoPay) and Brazil (Pix → Pix Automático) shows where consolidated scheme governance tends to go.

India: UPI AutoPay's rapid ascent

UPI's infrastructure was designed for push transfers — scan a QR, send money. The mandate layer came later, and it is growing faster than almost anyone anticipated.

UPI AutoPay (part of UPI 2.0, operated by NPCI) enables recurring debit mandates directly from a UPI-linked bank account. The mandate setup:

- Merchant presents a registration request (via UPI deep link or collect flow)

- Customer authenticates once with their UPI PIN in their banking app (PhonePe, Google Pay, Paytm, etc.)

- Mandate is stored in NPCI's infrastructure

- On each billing cycle, the merchant's PSP triggers a debit instruction

- The customer receives a pre-debit notification (PDN) at least 24 hours before each collection — they can block within that window

- If no action is taken, the debit executes automatically

This 24-hour veto window is structurally different from SEPA Direct Debit, where the consumer's refund right is post-debit. Every UPI AutoPay collection is individually veto-able by the customer. In practice, block rates are low, but it creates a consumer protection layer that affects how operators model recovery rates.

Growth data: UPI AutoPay processed 175 million transactions in January 2025, up 3× from 58 million in January 2024. New mandates created reached 35 million in January 2025, more than double the 14.5 million a year earlier. UPI AutoPay holds an estimated 53% share of all recurring payment transactions in India as of early 2025, overtaking card-based mandates.

This growth is partly regulatory in origin. The RBI's 2020–2022 enforcement of additional factor authentication for recurring card payments above ₹5,000 (later revised to ₹15,000) disrupted card standing instructions at scale — millions of merchant-initiated card mandates failed during migration. The India RBI tokenization mandate reshaped card token management at the same time. UPI AutoPay, being bank-native with authentication built into mandate setup, absorbed much of that displaced volume.

Transaction limits (current):

Standard recurring categories (OTT, SaaS, utilities, mobile bills): ₹15,000 per debit. Above this threshold, customers must enter MPIN for each transaction — effectively removing the automatic mechanism. For standard-category B2B SaaS pricing above approximately USD 180/month at current rates, UPI AutoPay does not work without per-debit customer action.

Elevated categories per NPCI Circular UPI-OC-151A (December 2023): insurance premiums, mutual fund SIPs, credit card bill payments, and loan EMIs qualify for ₹1,00,000 per debit without per-debit MPIN entry.

International SaaS companies billing in USD with no Indian entity are generally not on UPI AutoPay — they use card-on-file through a global PSP or a local payment aggregator (Razorpay, PayU, Cashfree) that handles the Indian entity and regulatory requirements. NACH/eNACH remains the alternative for cases where UPI AutoPay's ₹15k cap is the binding constraint, with 2-5 day activation and no practical upper limit.

Europe: SEPA Direct Debit's commercial risks

SEPA Direct Debit is the mature end of this spectrum — over a decade of operating history, high success rates, and deep PSP support through GoCardless, Stripe, Mollie, and others. The 2025 SDD Core Rulebook v1.0 entered force on October 5, 2025.

The European Payments Council operates two SDD schemes. The distinction matters for subscription operators.

SDD Core: Consumer-facing. The merchant holds the mandate — the bank does not pre-validate it. Key consumer protection: 8-week no-questions-asked refund right. The payer can instruct their bank to reverse a collection within 8 weeks, and the bank must comply without requiring justification. After 8 weeks and up to 13 months, refund rights apply only to unauthorized transactions. Settlement takes D+1 to D+5 business days.

SDD B2B: Business-to-business only. The payer's bank must pre-validate that a mandate exists before executing the debit. No consumer refund right — the payment is final 3 business days after collection. Settlement D+1. Mandate pre-registration with the debtor's bank limits access but significantly improves collection reliability.

The 8-week refund right on SDD Core is the most significant commercial risk for SaaS operators. A customer can reverse a charge without explanation months after receiving service. In practice, dispute rates on well-managed SDD portfolios are low — success rates above 98% are typical. But it creates an asymmetric exposure that doesn't exist on UPI AutoPay (where the consumer veto is pre-debit) or Pix Automático.

SCA exemption: One of SDD's structural advantages over card recurring payments in Europe is that it is entirely exempt from Strong Customer Authentication under PSD2/SCA. The mandate setup involves authentication at signing; subsequent debits are treated as mandated by that initial consent, with no recurring 3DS challenge. Card-on-file recurring payments require the MIT exemption framework, and the initial charge requires 3DS-authenticated setup. The authentication overhead and its conversion impact is covered in the 3DS2 analysis — for recurring billing specifically, SDD Core avoids it entirely.

The EU Instant Payments Regulation mandating SCT Inst at standard pricing is a separate development — SCT Inst remains push-based and does not add pull capability. UK open banking VRPs (Variable Recurring Payments) are developing as a bank-account debit mechanism with tighter controls than SDD, but UK VRP operates on a separate post-Brexit timeline from the SEPA schemes.

Brazil: Pix Automático — real-time pull

Pix is the most used payment method in Brazil — 6.3 billion transactions in March 2025 alone, on track for approximately 8 billion monthly by end of 2025. It holds roughly 40% of Brazilian e-commerce payment volume, and 61% of EBANX-processed SaaS revenue from Brazil flows through Pix. Pix launched as a push rail. Every transaction required manual payer initiation. For subscriptions, operators relied on boleto (barcode invoice requiring manual payment each cycle, settled in 1-3 days) or card-on-file. Boleto requires customer action on every billing date. Cards don't reach the roughly 60% of Brazilians without credit cards.

Pix Automático is BCB's answer, launched June 16, 2025 — a pull-debit layer on the existing Pix infrastructure, with instant settlement.

How authorization and collection work:

- Merchant's PSP sends a recurrence record (payer identity, schedule, fixed or variable amount) through BCB's infrastructure to the payer's PSP

- Payer receives a push notification in their banking app and authorizes the recurrence with a single confirmation — two consent journeys are supported (push notification approval or QR code scan)

- Once authorized, subsequent debits execute automatically on each billing date

- BCB requires collections to be scheduled 2–10 days before the due date

- Settlement occurs via Pix rails in seconds; payer receives real-time confirmation in their banking app

- Payer can cancel at any time through a BCB-mandated dedicated section in their bank app

The comparison to boleto is stark. Boleto requires manual payer action every cycle, settles in 1-3 days, and has no automated retry for non-payment. Pix Automático is fully automated after setup and settles instantly. For recurring billing, boleto's only remaining use case is one-time large B2B invoices and first-time checkout for users without Pix-connected accounts.

Early PSP integrations are live through EBANX (primary route for international merchants), PagBrasil, and PayRetailers. FastSpring began adding Pix Automático support for digital goods merchants. Full international merchant rollout through Q3 2025 was the projected timeline at launch.

When card-on-file still wins

Three structural reasons explain why a cross-border SaaS operator building a global subscription product still starts with card-on-file:

Entity requirements. eGIRO requires a Singapore bank account. UPI AutoPay mandate creation flows through locally registered Indian payment aggregators. Pix Automático channels through Brazilian PSPs. SEPA SDD requires a Creditor Identifier from a SEPA banking relationship. Card-on-file through Stripe, Adyen, or a Merchant of Record requires none of this.

Mandate portability. If you switch PSPs, card tokens can be migrated — with friction that depends on your tokenization approach, but the path exists. Bank debit mandates are typically tied to the PSP that created them. A PSP switch can mean re-authorizing every mandate, which is existential churn risk for a subscription business at scale.

Card network updater services. Visa Account Updater and Mastercard ABU automatically push new card details to merchants when cards are reissued. There is no equivalent for bank debit — a closed account or changed IBAN requires mandate recreation with customer action.

The calculus shifts when you have local entity presence, meaningful local volume, and the dunning infrastructure to handle market-specific failure modes. At that point, layering eGIRO for Singapore, UPI AutoPay for India under ₹15k, SDD Core for Europe (B2B where relevant), and Pix Automático for Brazil alongside card-on-file reduces per-transaction cost materially and opens the unbanked addressable market.

Multi-acquirer routing and payment orchestration architectures — where you route across payment methods based on cost and authorization rates — are the infrastructure layer that makes running multiple billing rails practical. Adding a local recurring rail is structurally similar to adding a second acquirer: the routing logic determines when to prefer the local rail over card, and the dunning stack manages the different failure modes in parallel.

The operator decision matrix

The direction is clear: real-time rails are growing pull-payment capabilities, activation friction is dropping, and the cost advantage over cards is being exposed as a competitive lever. UPI AutoPay's volume tripled in twelve months. Pix Automático is live and PSP integrations are expanding. SPaN consolidation suggests PayNow's mandate layer is a policy decision rather than an architectural impossibility.

The question for subscription operators is no longer whether to add local rails — it is which markets have crossed the threshold where entity footprint and volume justify the infrastructure investment.

For Singapore PayNow use cases specifically — the corporate guide covers the full PayNow feature set including QR collection and API flows, which are relevant for one-time checkout even where subscription billing requires eGIRO.

Sources & methodology (9)

UPI AutoPay hit 175 million transactions in January 2025, up 3× from 58M in January 2024

Checked:

UPI AutoPay holds 53% share of all recurring payment transactions in India as of early 2025

Checked:

NPCI Circular UPI-OC-151A sets ₹1,00,000 limit for insurance, SIPs, loan EMIs, and credit card bill payments

Checked:

MAS and ABS announced Singapore Payments Network (SPaN) in February 2025, incorporated June 2025

Checked:

Pix Automático launched June 16, 2025, operated by BCB

Checked:

Pix processed 6.3 billion transactions in March 2025; on track for ~8 billion monthly by end of 2025

Checked:

61% of EBANX-processed SaaS revenue in Brazil flows through Pix

Checked:

SEPA SDD Core 2025 Rulebook v1.0 entered force October 5, 2025; 8-week no-questions-asked refund right codified

Checked:

eGIRO digital mandate activates in minutes for individuals vs 21 working days for paper GIRO

Checked:

Source types explained in our Methodology.