SEPA Credit Transfer, Instant, and Direct Debit: Operator Guide

SEPA payments explained for operators: SCT, SCT Inst, and SDD Direct Debit, with scheme coverage, timing, fees, and merchant use cases.

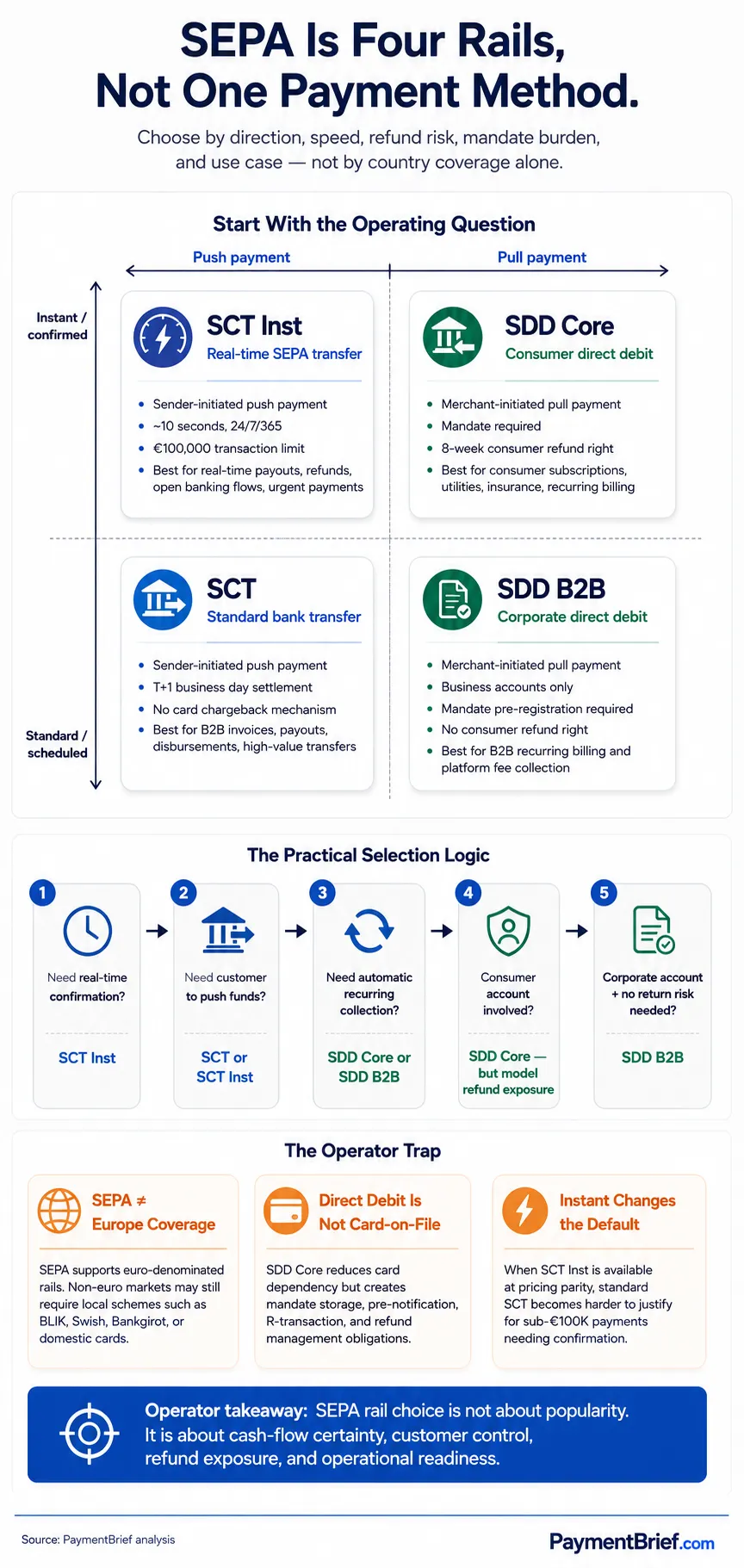

Four SEPA schemes, 36 countries, one reference. SCT Inst mandatory for eurozone PSPs since Oct 2025. SDD Core carries an 8-week consumer refund right. IBAN name check mandatory from Oct 2025. SEPA ≠ euro — 16 non-eurozone members use national schemes for local currency.

SEPA encompasses four payment schemes across 36 countries: SEPA Credit Transfer (SCT, push payment, T+1), SEPA Instant Credit Transfer (SCT Inst, 10 seconds, mandatory for eurozone PSPs since October 2025), SEPA Direct Debit Core (SDD Core, pull payment, 8-week consumer refund right), and SEPA Direct Debit B2B (SDD B2B, corporate pull payment, no refund right). The right scheme depends on payment direction, settlement urgency, counterparty type, and whether chargeback-equivalent protection is needed. SEPA ≠ euro: 16 SEPA members are not in the eurozone and use national schemes for local currency transactions.

Most operators treating Europe as a single payment market default to card. The result: interchange on every consumer transaction, SCA friction on every checkout, and no leverage over card network cost increases. SEPA offers a different economics entirely — near-zero MDR, irrevocable push payments, and a pull payment mechanism that handles subscription billing without card expiry risk. The tradeoff is operational complexity: four schemes, each with different settlement mechanics, refund rules, and integration requirements.

This guide covers all four SEPA schemes as an operator reference — when to use each, how the operational mechanics work, and what the 2025 regulatory changes mean for anyone processing euro payments.

The Four Schemes at a Glance

All four settle in euros. All require IBAN-formatted bank account identifiers. None involve card networks — no interchange, no scheme fees, no card network rules.

SEPA Credit Transfer (SCT)

SCT is the eurozone's standard bank transfer — the equivalent of a domestic wire, but standardised across 36 countries under a single rulebook. A German merchant receiving payment from a French customer gets the same format, the same IBAN structure, and the same settlement timeline as a payment from a Dutch customer.

How it works: The payer's bank formats an ISO 20022 credit transfer message and submits it to EBA Clearing's STEP2 system or an equivalent clearing infrastructure. STEP2 nets positions across participating banks and settles in central bank money at the designated settlement windows (currently multiple times per business day). Funds arrive T+1.

Key characteristics:

- No chargeback mechanism: SCT payments are irrevocable once the funds leave the sender's account. Unlike card payments, there is no network-level dispute process. Fraud recovery requires civil action or direct negotiation.

- No transaction limit for practical purposes: The scheme supports up to €999,999,999.99 — effectively unlimited for any legitimate commercial use.

- Operating hours: SCT processes during business hours on TARGET2 settlement days. Payments submitted on Friday afternoon may not settle until Monday.

When to use SCT: B2B invoice settlement where T+1 is acceptable, marketplace and platform payouts to sellers, payroll for European employees, and high-value consumer purchases where the customer initiates the payment directly from their bank.

SEPA Instant Credit Transfer (SCT Inst)

SCT Inst is SCT with real-time settlement — the same push payment mechanics, but settling in under 10 seconds, 24/7/365 including weekends and holidays. Since October 9, 2025, SCT Inst has been mandatory for all eurozone PSPs under the EU Instant Payments Regulation — and critically, mandatory at the same price as or lower than standard SCT.

The pricing parity rule changes everything. Before the IPR, many PSPs charged a premium for instant settlement — €0.20 standard vs €0.40 instant, for example. That differential is now prohibited. The practical consequence: there is no longer a cost reason to use standard SCT over SCT Inst for any payment where both sender and recipient PSPs support it. Instant is the new default.

Infrastructure: SCT Inst routes through RT1 (EBA Clearing's instant payment platform) or TIPS (the ECB's TARGET Instant Payment Settlement system). Both provide final, irrevocable settlement in central bank money within the 10-second window.

Transaction limit: the former €100,000 scheme-level cap was removed by the EU Instant Payments Regulation (5 October 2025); PSPs now set their own per-transaction limits. In practice most consumer and B2B use cases settle well within whatever limit a given PSP applies.

IBAN name check: From October 2025, PSPs must verify that the account name provided by the sender matches the name registered to the IBAN before executing an outbound SCT or SCT Inst. This Verification of Payee (VoP) requirement is a fraud prevention measure — authorised push payment (APP) fraud where attackers trick senders into misdirecting payments. Operationally, any payout workflow needs a name-check API call before executing the transfer.

SEPA Direct Debit Core (SDD Core)

SDD Core is the consumer-facing pull payment mechanism — the merchant initiates the debit, not the customer. It is the SEPA equivalent of UK Direct Debit, and it powers most recurring billing, utility collection, and subscription charging in the eurozone.

The Mandate Lifecycle

SDD Core requires a signed mandate from the customer before any debit can be initiated. The mandate authorises the merchant (the "creditor") to collect specific payments from the customer's account. Every mandate must include:

- Unique Mandate Reference (UMR): Assigned by the merchant, must be unique per customer-creditor pair

- Creditor Identifier (CI): The merchant's SEPA registration identifier, obtained from the national scheme manager

- Creditor name and address

- Debtor's IBAN and BIC

- Type of payment (recurrent or one-off)

- Customer signature (wet or electronic)

The mandate lifecycle has five operational steps:

- Collection: Mandate signed by customer at account setup. Electronic mandates (via online checkout) are common and valid under EPC rules — the mandate reference and acceptance timestamp must be stored.

- Storage: Merchant retains the mandate. Unlike UK Direct Debit where Bacs holds mandate data, SEPA mandates are held by the creditor. Storage and retrieval are the merchant's responsibility.

- Pre-notification: Merchant must notify the customer of the upcoming debit at least 14 days before the collection date — unless a shorter period is agreed in the mandate. The notification must include the amount and collection date. Most subscription platforms reduce this to 1–3 days by agreement in their terms.

- Collection submission: Merchant submits the debit instruction to their bank. Submission deadlines vary by bank — typically D-1 or D-2 before the collection date for first-time debits, D-1 for recurring.

- Settlement: Funds transfer T+1 to T+3 after the collection date.

R-Transactions

Any SDD collection that does not complete generates an R-transaction. There are five types and they are not interchangeable in reconciliation:

- Reject (before settlement): Bank refuses to execute — closed account, insufficient funds, mandate not found. Returns within D+1.

- Return (after settlement, bank-initiated): Bank reverses after settlement for technical reasons. Returns within 5 business days.

- Refund (after settlement, debtor-initiated): Customer exercises the 8-week refund right. Debtor's bank reverses without requiring justification.

- Reversal (after settlement, creditor-initiated): Merchant cancels the collection after it has settled — to correct an error. Must be within 5 business days.

- Refusal (before settlement, debtor-initiated): Customer instructs their bank to refuse a specific collection before it executes.

The 8-week refund right is the SDD Core characteristic that most affects merchant revenue recognition. Any consumer can request a full refund of any SDD Core debit within 8 weeks of the settlement date, no questions asked. For digital subscription services, this creates a potential 8-week revenue reversal window on every collection. Merchants with high-value subscriptions or services where customers historically dispute need to model this exposure explicitly.

SEPA Direct Debit B2B (SDD B2B)

SDD B2B is the corporate variant. The mechanics are similar — pull payment, mandate required, merchant-initiated — but with three critical differences:

No consumer refund right: Once an SDD B2B debit settles, the debtor's bank cannot initiate a refund on the debtor's behalf. The irrevocability is equivalent to a credit transfer. This makes SDD B2B suitable for B2B invoice collection where the 8-week return window of SDD Core would create unacceptable working capital uncertainty.

Mandate pre-registration with debtor's bank: Before the first SDD B2B collection, the mandate must be registered with the debtor's bank. The debtor authorises their bank to accept debits from the specific creditor (identified by Creditor ID). Banks are required to verify each incoming SDD B2B debit against their registered mandates and block unrecognised collections. This pre-registration step adds friction to onboarding but eliminates the fraud and error risk of unverified pull payments.

Faster bank confirmation: SDD B2B debit instructions submitted D-1 settle T+1 with bank confirmation available before settlement — earlier than SDD Core. For cash flow management, this is operationally meaningful.

Restriction to businesses: SDD B2B is only available for transactions between business accounts. Consumer accounts cannot be debited via SDD B2B — the scheme rules require both parties to be non-consumers.

IBAN Name Check (Verification of Payee)

From October 2025, the Instant Payments Regulation requires all PSPs to verify that the IBAN and account holder name provided by the payer match before executing an outbound SCT or SCT Inst.

How it works: The sending PSP queries the receiving PSP's Verification of Payee API with the intended IBAN and the payee name the sender provided. The receiving bank returns one of three responses: match, close match (name differs slightly — typo or nickname), or no match. If the result is no match, the PSP must alert the sender before proceeding.

Operational implications for merchants:

- Any payout workflow (marketplace disbursements, refunds, B2B payments) needs to integrate VoP before execution

- VoP adds one API round-trip to the payment flow — latency consideration for real-time payout products

- PSPs (Stripe, Adyen, GoCardless) are building VoP into their APIs; direct bank integrations require explicit implementation

- False positives (close match responses for legitimate payees with name variations) need a UX flow that lets the sender confirm and proceed

The 36-Country Trap: SEPA ≠ Euro

SEPA has 36 member countries but only 20 are in the eurozone. The remaining 16 — including Sweden, Denmark, Norway, Switzerland, Poland, Hungary, Czech Republic, Romania, Bulgaria, and the UK (partially) — are SEPA members, meaning their banks support euro-denominated SEPA transfers. But domestic consumers and businesses in these countries transact in local currency: SEK, DKK, NOK, CHF, PLN, HUF, CZK, RON, BGN, GBP.

SEPA rails cannot be used for local-currency transactions in these countries. An operator collecting subscription payments from Polish consumers in PLN needs BLIK or local card acceptance — not SEPA Direct Debit. A Swedish consumer paying in SEK uses Swish or Bankgirot, not SCT Inst.

The practical trap: operators who assume "we support SEPA so we cover Europe" have zero coverage for local-currency payments in half of the EU's member states. The eurozone/non-eurozone distinction needs to drive payment method routing logic explicitly.

Which Scheme for Which Use Case

| Use Case | Recommended Scheme | Reason |

|---|---|---|

| Consumer subscription (monthly) | SDD Core | Pull payment, automatic, 8-week return is acceptable |

| B2B SaaS billing (annual invoice) | SDD B2B or SCT | B2B has no refund right; SCT works if customer pushes payment |

| Marketplace seller payout | SCT Inst | Real-time settlement, no limit for amounts under €100K |

| Customer refund | SCT Inst | Fastest resolution, improves customer experience |

| High-value B2B invoice (>€100K) | SCT | Only scheme supporting amounts above €100K |

| Open banking payment initiation | SCT Inst | Settlement rail under most PSD2/PSD3 PISP flows |

| Utility and insurance billing | SDD Core | Established consumer expectation, mandate reuse across billing cycles |

| Platform fee collection from business accounts | SDD B2B | No return risk, mandate pre-registered, irrevocable |

For how SEPA Instant interacts with open banking payment initiation and Variable Recurring Payments, the VRP article covers the UK analogue in detail — the settlement economics and mandate structure are similar in intent though different in implementation. For the full compliance picture on the Instant Payments Regulation and what it requires of PSPs, the EU Instant Payments Regulation deep dive covers the operational obligations. For subscription billing that spans SEPA markets and beyond — India, Brazil, Southeast Asia — the rail comparison article maps the full landscape.

Sources & methodology (8)

SEPA Credit Transfer Rulebook — scheme rules, ISO 20022 format, settlement via STEP2

Checked:

SEPA Instant Credit Transfer mandatory for all eurozone PSPs from October 9, 2025 — EU Regulation 2024/886

Checked:

SDD Core 8-week refund right for authorised transactions; 13 months for unauthorised

Checked:

IBAN name check (Verification of Payee) mandatory for outbound SCT and SCT Inst from October 2025

Checked:

Stripe SEPA Direct Debit — mandate collection, pre-notification, SDD Core and B2B

Checked:

GoCardless SEPA Direct Debit — mandate lifecycle, Creditor ID, R-transactions

Checked:

SEPA covers 36 countries; 20 eurozone members; the former €100,000 SCT Inst scheme-level cap was removed under the EU Instant Payments Regulation — PSPs now set their own per-transaction limits

Checked:

Adyen SEPA Direct Debit — mandate management, SDD B2B, pre-registration requirement

Checked:

Source types explained in our Methodology.