AI Chargeback Representment Automation: What Actually Works in 2026

The global chargeback burden hit $33.8B in 2025, but merchants net only 8.1% on representment. Here's where AI automation changes the math and where it doesn't.

Friendly fraud at 44% baseline is the automation target; fraud chargebacks at 17.1% are not. AI lifts win rates from 20–40% manual to 65–80%. CE 3.0 auto-qualification (Oct 2025) + VAMP enforcement changed the ROI calculus.

AI chargeback representment automation improves win rates from 20-40% (manual) to 65-80% on friendly fraud disputes, reduces per-dispute handling cost from $25-50 to $3-8, and is now materially more valuable because CE 3.0 auto-qualification and VAMP enforcement both took effect in late 2025.

Global chargebacks reached $33.8 billion in value in 2025 — 261 million transactions, a cost multiplier of $3.75 to $4.61 for every $1 lost when you account for fees, merchandise, and operational overhead. The number that matters more for operators is this: merchants net 8.1% through representment (Chargebacks911 Field Report 2024). That is not an automation problem. It is a structural problem that automation makes incrementally better, and only on certain dispute types.

Vendors selling AI representment automation will show you win rates of 65–80%. Those numbers are real for the disputes they are winning. What they do not surface upfront: a 17.1% baseline win rate on fraud chargebacks, where automation mostly reshuffles a bad hand. The difference between operators who buy automation and see results and those who buy it and see marginal improvement is almost always whether they knew their dispute mix before they bought.

This article covers the mechanics of what AI representment actually does, where the vendor market sits, how to read the win rate math, and the two regulatory changes from late 2025 — CE 3.0 auto-qualification and VAMP enforcement — that fundamentally changed the ROI calculation.

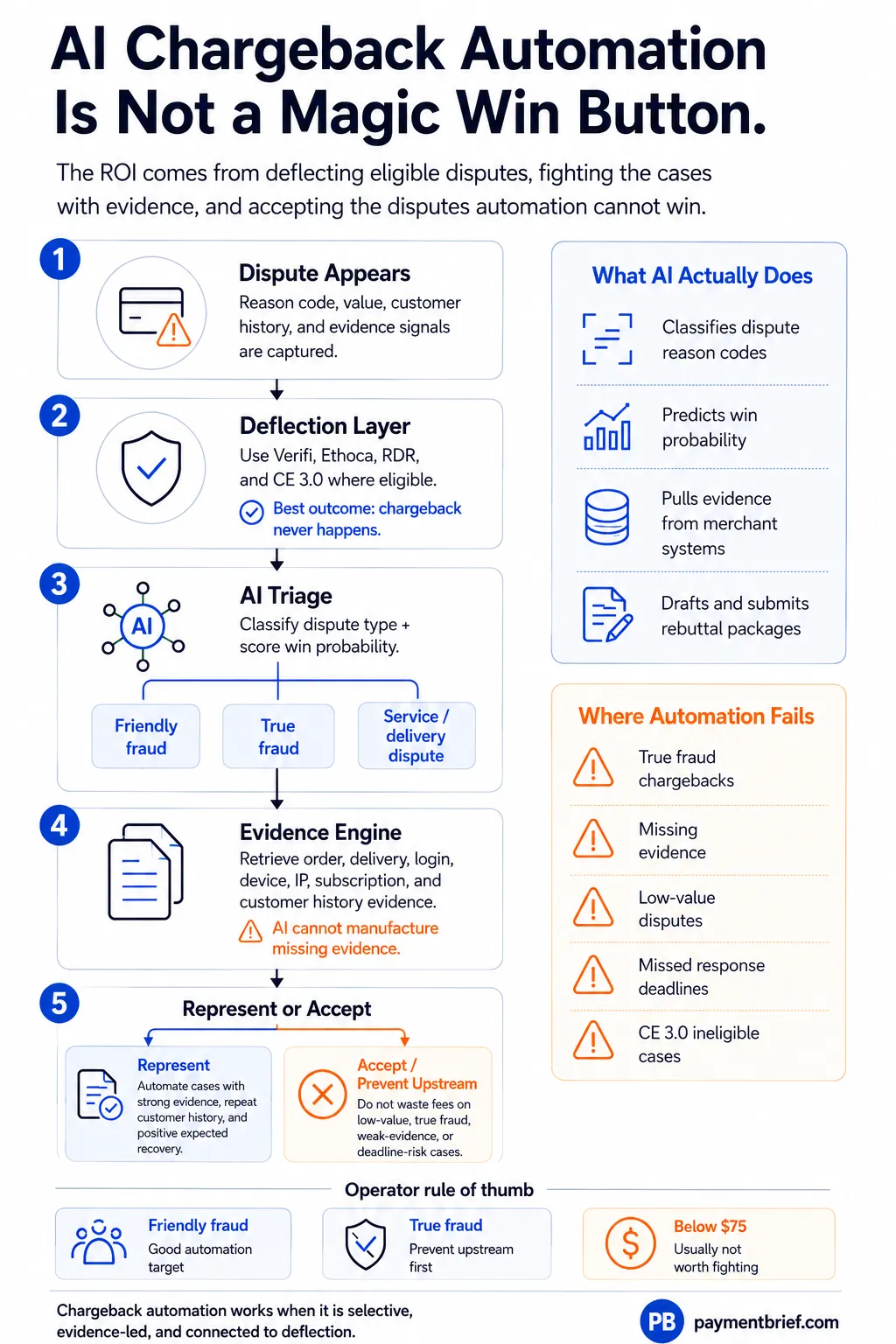

What AI representment actually does

Most operators conflate two distinct tools: dispute deflection and representment automation. They are not interchangeable.

Dispute deflection operates pre-chargeback. When a cardholder contacts their issuer to dispute a transaction, Verifi Order Insight and Ethoca Consumer Clarity push enriched merchant transaction data — itemized receipts, delivery confirmations, subscription terms, logo, customer service contact — directly into the issuer's interface. The issuer can resolve the dispute at that moment without ever issuing a chargeback. For merchants with the right transaction data infrastructure, this is the highest-ROI intervention in the dispute lifecycle. Ethoca Consumer Clarity prevents up to 23% of chargebacks on average, and up to 70% in certain verticals (primarily subscription and digital goods). Verifi Order Insight claims up to 70% dispute prevention for eligible transactions. These numbers reflect deflection — the chargeback never happens.

Representment automation operates post-chargeback. The chargeback has already been issued, the merchant account has been debited, and the clock is running. AI representment systems do three things in this phase: they classify the dispute by reason code and predict its win probability, they retrieve and assemble the evidence package appropriate to that reason code, and they draft the rebuttal letter and submit the package to the acquirer within the deadline window.

The distinction matters operationally because the tooling, integrations, and cost structures are different. Deflection tools require real-time data feeds — merchant systems must be able to serve up transaction metadata on demand when issuers query. Representment tools need access to order management systems, carrier APIs, login event logs, and fraud platform data to pull the evidence retroactively. Operators who try to solve a representment problem with deflection tools (or vice versa) get the wrong answer.

For a detailed walkthrough of the dispute lifecycle stages and reason code evidence requirements, the chargeback representment guide covers that mechanics layer.

The vendor map

The representment automation market has consolidated around a handful of platforms with distinct positions in the stack. This vendor map covers the representment-automation layer specifically; for the full operating-model comparison — pre-dispute alert networks, representment automation, and managed recovery as one stack — see Chargeback Management Compared: Alerts, Representment, and Recovery Models.

Stripe Chargeback Protection is a liability transfer product, not a representment tool. At 0.4% per eligible transaction, Stripe absorbs the dispute and reimburses the merchant up to a $25,000 annual cap — but only for fraud disputes. "Product not received" and "not as described" chargebacks are explicitly excluded. Stripe integrates both Verifi and Ethoca on the deflection side, which is the actual value for most merchants. For operators who want certainty on fraud disputes and are already on Stripe, the 0.4% fee is straightforward to evaluate against their fraud rate. For operators whose dispute mix skews toward non-fraud reason codes, Stripe Chargeback Protection does not address the problem.

Sift Dispute Management uses ML-powered Response Recommendations to automate representment workflows. Sift acquired Chargeback (the company) in 2021 and integrated its dispute automation capabilities into the Sift platform. It connects natively with Adyen and PayPal, making it a natural fit for operators on those acquirers. The product automates evidence gathering and response filing; the ML layer predicts win probability per dispute and can route low-probability cases to acceptance rather than burning time on unwinnable fights.

Adyen Protect and Disputes API takes a different approach: Adyen automatically defends applicable chargebacks with no merchant action required for disputes that meet its criteria. The Chargeback Uploader allows merchants using Adyen for processing but external acquirers for other channels to submit evidence through a single interface. For merchants whose primary acquirer is Adyen, this is the lowest-friction path to automated defense.

Chargebacks911 UDMS and ResolveLab represent the highest automation ceiling in the market — 98% automation using AI-powered robotics, a number Chargebacks911 has been citing since 2022 for their Unified Dispute Management System. ResolveLab specifically addresses the evidence quality problem for friendly fraud: it captures consent and permission trails at the point of transaction (opt-in confirmations, click-through records, session data) and makes that evidence retrievable later. This is important because friendly fraud representment wins require showing that the customer authorized the transaction and received what they paid for, which requires documentation captured at transaction time, not assembled retroactively.

Verifi Order Insight (Visa/Verifi) and Ethoca Consumer Clarity (Mastercard) are the deflection layer. Verifi's CE 3.0 integration enables merchants to share login details, IP addresses, device IDs, and delivery confirmations in real time with issuers. Ethoca's single integration covers both Visa and Mastercard deflection signals. For operators who are not yet on either network, this is the first integration to prioritize — preventing a chargeback is materially cheaper than winning one.

Midigator occupies the analytics-driven end of the market: data-analytics-first (classic ML, not LLM-generated responses), customizable evidence templates, and a focus on dispute segmentation before automation. Midigator's 65–80% win rate is its headline number; the operational context is that it achieves this by being selective about which disputes it contests.

The win rate math

The 45% industry average win rate for representment is an aggregate that obscures the underlying dispute type variance. Building an automation strategy on the aggregate number is how operators end up buying tooling for disputes they cannot win.

Manual in-house representment achieves 20–40% win rates. AI-assisted platforms reach 65–80% on the disputes they target. The gap is real — but the question is which disputes those win rates reflect.

Friendly fraud disputes — where a cardholder disputes a legitimate transaction — have a 44% baseline win rate. This is the target population for representment automation. The evidence profile is predictable: delivery confirmations, login logs, prior transaction history, behavioral data. Automation systems are good at retrieving structured evidence against a defined template. The pattern is consistent enough that ML models can accurately predict win probability before filing, and LLMs can assemble coherent rebuttal narratives from the raw evidence.

Fraud chargebacks — where a card was genuinely compromised — have a 17.1% baseline win rate. These are a fundamentally different problem. The merchant often cannot prove the legitimate cardholder authorized the transaction, because they did not. Automation does not meaningfully improve outcomes here. Deploying automated representment against a predominantly fraud-driven dispute mix is spending $3–8 per dispute to lose.

High-value transactions (above $300) achieve only a 28% win rate even with a complete evidence package. Issuers apply higher scrutiny, cardholders are more motivated to pursue disputes, and the evidence requirements become more demanding. Automation helps on volume; it does not solve the intrinsic difficulty of high-value dispute defense.

Operators who measure dispute type before buying automation and see that their fraud chargeback rate is 60%+ of their mix should invest in fraud prevention (reducing the chargebacks) before they invest in representment automation (fighting the chargebacks). The AI fraud detection article covers that layer specifically.

LLM vs ML: the hybrid that actually works

No major vendor publishes their model architecture. What is consistent across public documentation, vendor case studies, and operator conversations is the pattern: hybrid is the standard, not the exception.

The ML layer handles structured prediction tasks: dispute classification by reason code, win probability scoring based on available evidence signals, routing decisions (contest vs. accept), and escalation triggers. Classic ML — gradient boosting, decision trees, ensemble models — is better suited to tabular feature scoring than LLMs. It runs faster, is more explainable (relevant when acquirers ask why a case was filed), and produces stable outputs on structured data. Midigator's approach is explicitly data-analytics-driven, which reflects a deliberate architectural choice against LLM-generated responses.

The LLM layer handles natural language tasks: converting raw structured evidence (carrier tracking confirmations, login timestamps, session data) into coherent rebuttal narratives that meet the acquirer's submission format. Assembling a compliant representment letter from a delivery API response, a fraud platform risk score, and IP log data is exactly the type of unstructured synthesis task LLMs do well. The output is auditable, the evidence is grounded in real data, and the generation process is faster than a human analyst by orders of magnitude.

The rule engines vs ML architecture piece covers the underlying hybrid design in depth; the same structural logic applies to dispute systems. Rules govern action limits (when to accept, when to escalate to pre-arbitration), ML scores the probability distribution, and where natural language output is required, LLMs handle generation. The automation ROI comes from eliminating the human-in-the-loop for the structured 70–80% of cases while preserving human review for high-value or complex disputes.

Where automation fails

The five-to-ten working day practical response window is the most underestimated failure point. Nominal dispute response windows are quoted at 20–45 days depending on network and reason code. The practical window is 5–10 working days because acquirer processing queues, bank holidays, and submission format rejections consume time that the nominal deadline does not account for. Systems that wait for evidence retrieval to complete before initiating submission will miss deadlines on a portion of their case volume. Missed deadline equals automatic loss, no grace period, no appeal.

CE 3.0 has a specific evidence constraint that automation cannot solve retroactively: it requires two prior undisputed transactions that are 120 to 365 days older than the disputed transaction. For merchants with short customer lifespans or low repeat purchase rates, the required prior transactions simply do not exist for a material share of disputes. Systems that flag CE 3.0 eligibility without checking the prior transaction condition generate false confidence.

Dispute type scope is another ceiling. CE 3.0 applies only to Visa reason code 10.4 (Other Fraud: Card-Absent Environment). Automation tools that market CE 3.0 benefits to merchants with dispute mixes heavy in 13.x (service disputes), 13.1 (not received), or Mastercard codes are describing a capability that does not apply to those cases.

Evidence availability gaps kill win rates before the AI layer gets involved. If the merchant's order management system does not retain structured delivery data, if carrier tracking webhook integrations failed, or if login event logs are not retained for 18 months, the evidence retrieval step returns empty and the ML model is scoring on signal-poor features. Automation does not manufacture evidence — it retrieves and assembles it. Gaps in data retention infrastructure translate directly to lost cases.

Network tokens improve authorization rate data quality and reduce fraud chargebacks at the source, but they do not retroactively improve evidence for existing disputes. For the longer-term view on token infrastructure and dispute prevention, the network tokens article and the authorization optimization piece both address upstream prevention levers.

CE 3.0 auto-qualification changed the calculus

Visa Compelling Evidence 3.0 launched in April 2023. The October 17, 2025 change that matters for operators is auto-qualification: merchants on Visa Secure and Visa Data Only across all regions now qualify for CE 3.0 automatically, without manual filing, for Visa reason code 10.4 disputes.

Before October 2025, CE 3.0 was available but required explicit merchant opt-in and manual evidence submission through Verifi. That friction suppressed adoption — many merchants who had qualifying prior transaction data never received the benefit because the operational burden to claim it exceeded the willingness to act case by case.

Auto-qualification means that for eligible disputes, the CE 3.0 evidence check happens automatically. If the merchant has the two required prior undisputed transactions (same cardholder, 120–365 days old, matching device/IP/shipping profile), the dispute is resolved in the merchant's favor at the issuer level — the chargeback never progresses to chargeback representment. The deflection happens earlier in the lifecycle, at lower operational cost than a representment filing.

The strategic implication: merchants on Visa Secure who have not audited their CE 3.0 eligibility rates are leaving automatic dispute resolution on the table. The first operational task is to determine what percentage of your Visa 10.4 disputes have qualifying prior transaction pairs. That percentage represents a dispute deflection rate you may already be capturing without realizing it — or that you should be capturing if your Verifi integration and transaction data retention are properly configured.

CE 3.0 resolutions do not count toward VAMP thresholds. That accounting treatment is what makes CE 3.0 particularly valuable for merchants approaching monitoring thresholds — each CE 3.0 resolution is a chargeback avoided that does not register in the ratio calculation.

VAMP replaced VDMP/VFMP — the stakes are higher

Visa retired VDMP and VFMP on March 31, 2025 and consolidated them into VAMP (Visa Acquirer Monitoring Program), effective April 1, 2025. The operational shift is significant.

VAMP enforcement at the Excessive level began October 1, 2025: $8 per transaction for merchants above the Excessive threshold. Above Standard enforcement began January 1, 2026: $4 per transaction. The minimum transaction volume for monitoring qualification is 1,500 transactions (effective June 1, 2025) — meaning smaller merchants now enter the monitoring program at volumes where they may not have previously been tracked.

The merchant threshold is now 1.5% for North America, Europe, and Asia-Pacific — it dropped from 2.2% on 1 April 2026 (CEMEA remains 2.2%). Merchants who were at 1.8–2.0% and treating it as comfortable headroom now breach the threshold without changing their behavior.

The mechanism that directly affects automation ROI: RDR-resolved pre-disputes do not count toward VAMP ratios. CE 3.0 resolutions do not count. This means dispute prevention tools — Verifi Rapid Dispute Resolution and CE 3.0 qualification — are not just reducing dispute volume; they are keeping resolved disputes out of the ratio calculation that determines monitoring status and fee exposure.

The math: for a merchant processing 10,000 transactions per month with a 2.0% dispute rate, the difference between that 2.0% counting toward VAMP versus 1.4% after RDR and CE 3.0 resolutions is the difference between being in monitoring and not. At $4–$8 per transaction in fees, 60 transactions per month above the threshold is $240–$480 in monthly fees. Annualized, that justifies a meaningful investment in Verifi and CE 3.0 infrastructure.

The upstream fraud prevention investment also matters here. Velocity checks and behavioral fraud signals that reduce fraud chargebacks reduce the VAMP ratio input — the same disputes that automation struggles to win (17.1% fraud chargeback win rate) are the ones that count against the threshold. Preventing fraud chargebacks through detection and blocking is the most efficient path to threshold management.

What operators should actually do

Instrument your dispute mix before buying automation. Break out your chargebacks by reason code, dispute type (fraud vs. friendly fraud vs. service dispute), and transaction value tier. If your fraud chargeback share is above 40% of volume, the ROI case for representment automation is weak. If your friendly fraud share is above 50%, automation should pay for itself quickly.

CE 3.0 is free if you are already on Visa Secure. Audit your Verifi Order Insight integration and transaction data retention first. Auto-qualification as of October 2025 means your existing infrastructure may already be deflecting eligible Visa 10.4 disputes. Confirm that your prior transaction data (two transactions per cardholder, 120–365 days old) is being retained and fed to Verifi correctly before spending on representment tooling for disputes that could be resolved at deflection.

Know your VAMP position. Map your current dispute ratio against the 1.5% threshold now in effect (2.2% in CEMEA). Identify how many disputes per month are resolved via RDR or CE 3.0 and thus excluded from the ratio. If you are within 0.5 percentage points of the threshold, your VAMP exposure should be a board-level conversation, not a back-office task.

Fix evidence retention before deploying automation. Automation systems retrieve evidence from your data sources — carrier APIs, order management systems, login event logs, fraud platform data. If those sources have gaps, the automation layer has nothing to work with. Audit your evidence availability by dispute type before signing vendor contracts. Carriers, authentication providers, and session event systems typically need 18 months of retention to cover the full range of dispute windows.

Separate the deflection and representment vendor decisions. Verifi Order Insight and Ethoca Consumer Clarity operate pre-chargeback. Representment platforms (Midigator, Chargebacks911 UDMS, Sift Dispute Management) operate post-chargeback. Stack them in order: deflect first, represent what gets through. Buying a representment platform and treating it as a deflection solution is spending on the wrong stage.

Do not automate disputes below $75. Even at $3–8 per automated dispute, the expected recovery on disputes below $75 with a 40–50% win rate is negative after acquirer fees and platform costs. Set a minimum transaction value threshold in your automation rules and accept below-threshold disputes. The operational discipline to accept strategically — rather than fight everything — is where operators recapture time and budget for the cases that move the number.

The $33.8B in global chargeback exposure is not going away. What has changed in the past 18 months is the tooling precision, the VAMP stakes that make threshold management unavoidable, and the CE 3.0 auto-qualification that makes deflection passive for eligible disputes. The operators who will see real improvement from automation in 2026 are the ones who enter it with a clean data picture, a segmented dispute mix, and a clear separation between deflection and representment in their stack.

Sources & methodology (8)

$33.8B global chargeback value in 2025 across 261M transactions

Checked:

8.1% merchant net win rate via representment

Checked:

Midigator 65-80% average win rate; manual in-house 20-40%

Checked:

Stripe Chargeback Protection: 0.4% per eligible transaction, $25,000 annual cap

Checked:

CE 3.0 auto-qualification launched October 17, 2025 for Visa Secure and Visa Data Only

Checked:

VAMP replaced VDMP and VFMP effective April 1, 2025; Excessive enforcement began October 1, 2025

Checked:

Ethoca Consumer Clarity prevents up to 23% of chargebacks overall, up to 70% in some industries

Checked:

Chargebacks911 UDMS: 98% automation with AI-powered robotics (2022)

Checked:

Source types explained in our Methodology.