AI Agents and Payment APIs: MCP, Stripe Agent Toolkit, and Mastercard

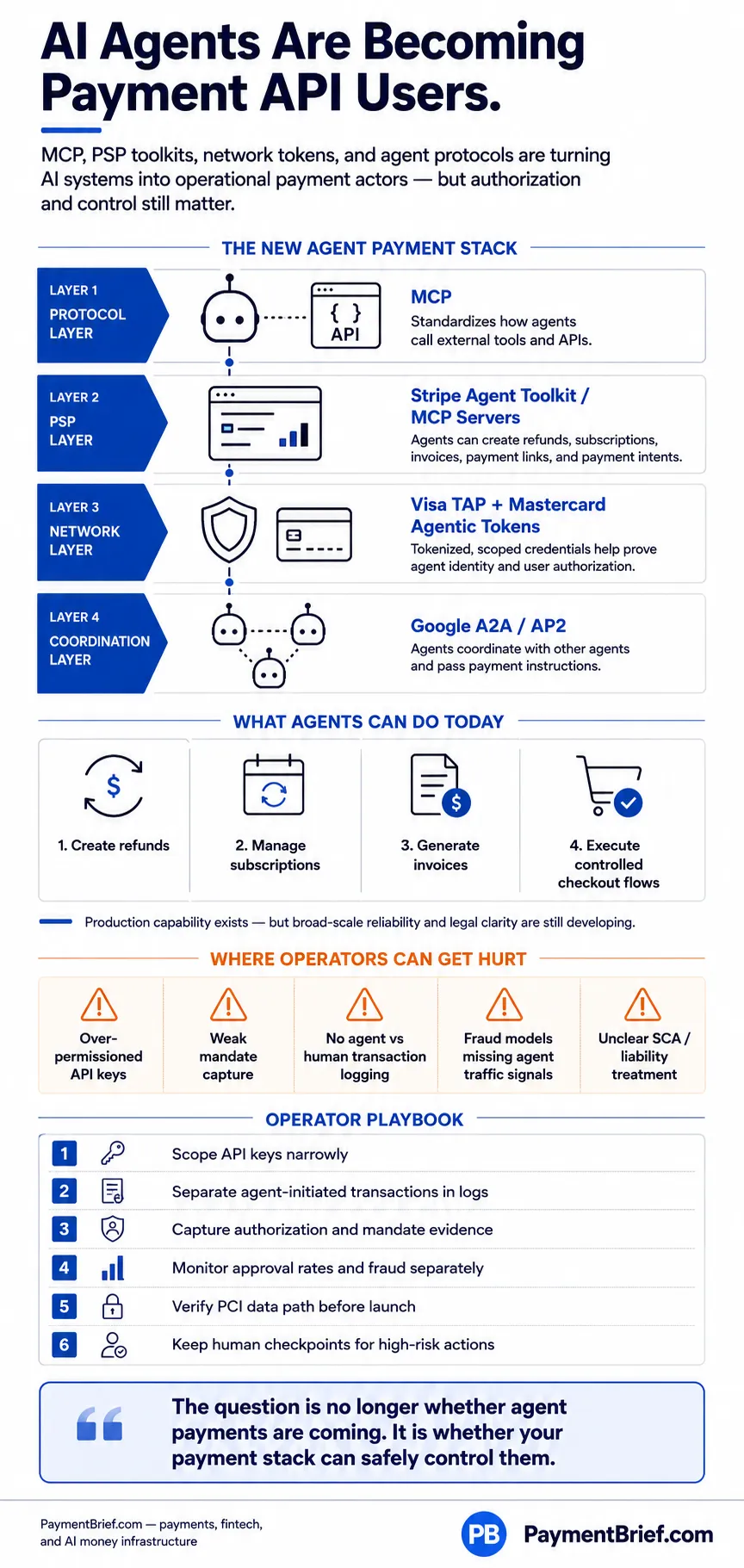

MCP, Stripe Agent Toolkit, Visa TAP, and Mastercard Agentic Tokens: four-layer stack covering protocol, PSP, and network layers for agentic commerce operators.

MCP: 97M monthly SDK downloads, donated to Linux Foundation Dec 2025. Stripe Agent Toolkit production — refunds, subscriptions, invoices via LLM. Visa TAP + Mastercard Agentic Tokens live. SCA regulatory gap for agent transactions unresolved in PSD3/PSR final text.

AI agents interact with payment APIs through three layers: the protocol layer (MCP, which standardizes how agents call tools), the PSP layer (Stripe Agent Toolkit, PayPal MCP, Square MCP — production today), and the network layer (Visa Intelligent Commerce + Trusted Agent Protocol, Mastercard Agent Pay + Agentic Tokens — live in controlled rollouts). Stripe's MCP server at mcp.stripe.com supports roughly 25 operations including refunds, subscription management, dispute listing, and invoice creation. Mastercard Agentic Tokens are per-agent scoped payment credentials — one token per AI service, with merchant-category and spend-cap constraints. Visa's Trusted Agent Protocol uses cryptographically signed HTTP messages to verify agent identity at checkout. Regulatory clarity on SCA for agent-initiated transactions is absent from PSD3/PSR final text as of April 2026.

The premise of agentic commerce — AI systems that purchase on behalf of users — moved from a theoretical scenario to a live transaction in 18 months. Mastercard confirmed Europe's first end-to-end payment executed by an AI agent in March 2026. Stripe's MCP server is OAuth-authenticated and handles roughly 25 payment operations in production. Visa's Trusted Agent Protocol has a GitHub repository and a developer spec that merchants can implement today.

The question for operators is no longer whether to take this seriously. It is whether you understand the stack well enough to build on it safely.

This article covers the four layers of the agent payment stack as it exists in mid-2026: the protocol layer (MCP), the PSP layer (Stripe, PayPal, Square), the network layer (Visa, Mastercard), and the coordination layer (Google A2A/AP2). For the broad AI payments infrastructure overview, the map article covers all layers at breadth. This goes deeper on the agent-specific integration reality.

The protocol layer: MCP

Model Context Protocol (MCP) was released by Anthropic on November 25, 2024. It was donated to the Agentic AI Foundation, a directed fund under the Linux Foundation co-founded by Anthropic, Block, and OpenAI, in December 2025 — removing single-vendor governance risk and placing it on the same institutional footing as Kubernetes.

By March 2026: 97 million monthly SDK downloads, 10,000+ public MCP servers, first-class support in Claude, ChatGPT, Cursor, Gemini, and VS Code.

What MCP actually is: A client-server protocol that standardizes how AI agents call external tools. MCP servers expose three primitives: Tools (executable functions — "create a refund"), Resources (readable data — "get customer profile"), and Prompts (templated instructions). AI clients call them. Think of MCP as the USB-C port for agent tool use — a single connector that any compliant server and any compliant agent can speak.

Why this matters for payment operators: Before MCP, integrating an AI agent with a payment API required custom function definitions per agent framework (OpenAI function calling format ≠ LangChain tool format ≠ Anthropic tool use format). An MCP server exposes the payment API once, and any MCP-compatible agent — across frameworks and models — can call it without per-integration custom code.

Stripe, PayPal, and Square have all published official production MCP servers. The payment ecosystem has effectively standardized on MCP as the agent integration layer.

The PSP layer: Stripe Agent Toolkit

Stripe's offering breaks into two components with different maturity levels.

The Agent Toolkit SDK (Python and TypeScript) is the developer integration path. It wraps Stripe's API as LLM-callable tools for OpenAI Agents SDK, LangChain, CrewAI, and Vercel AI SDK. What it can do in production today:

- Create, cancel, and retrieve subscriptions

- Create full or partial refunds (by charge ID or payment intent ID)

- Create and finalize invoices

- Generate payment links

- Create payment intents

- List and update disputes

- Create, update, and delete customers

- Retrieve real-time account balance

- Search Stripe's documentation (meta-tool for LLM self-help)

The MCP server at mcp.stripe.com exposes the same capabilities through the standard protocol, OAuth-authenticated. Current version v0.3.3 as of Stripe Sessions in April 2026.

Auth model: Stripe restricted API keys. You create a key scoped to exactly the operations your agent needs — a refund-only agent gets a key that can only call the refunds API. There is no per-agent token concept at the Stripe network level; scoping is your responsibility at the key management layer.

Agentic Commerce Suite (launched December 2025): A higher-level product targeting merchants who want to be discoverable and purchasable by AI agents. Components: an ACP (Agentic Commerce Protocol) endpoint per merchant at /api/acp exposing real-time product, price, and inventory data; a Checkout Sessions API handling shipping and taxes; Shared Payment Tokens for passing buyer credentials to merchants; and dedicated Agentic Fraud Protection tuned for non-human transaction patterns. Partners at launch include Wix, BigCommerce, commercetools, and Mirakl. OpenAI's "Instant Checkout" in ChatGPT runs on this infrastructure.

x402 machine payments (preview, not GA): Stripe, Coinbase, and AWS Bedrock AgentCore launched x402 in May 2026 — a revival of the HTTP 402 "Payment Required" status code for per-call USDC micropayments over Coinbase's Base L2. Designed for AI agents that need to pay for API access at the call level, without subscriptions. Preview status as of publication — do not build production infrastructure on this yet.

For the broader tokenization context that underpins these flows, the tokenization piece covers how stored credentials work at the PSP level.

The network layer: Visa Intelligent Commerce

Visa announced Intelligent Commerce on April 30, 2025 and launched the Trusted Agent Protocol (TAP) in October 2025 — an open framework (GitHub: visa/trusted-agent-protocol) built on existing web infrastructure.

How TAP works technically: Agent requests to merchants carry cryptographically signed HTTP messages using JWS (JSON Web Signatures). The signature contains the agent's identity, verified user authorization, and payment details. Merchants retrieve Visa public keys from a well-known URL and verify the signature. Crucially, the signature is bound to the merchant's specific domain and operation — preventing replay attacks and scope drift.

Why this matters for merchants: TAP lets you distinguish a legitimate credentialed AI agent from an anonymous bot and from malicious automation. Without it, agent-initiated traffic looks identical to bot traffic from a traditional fraud-detection perspective.

Consumer credential layer: Users enroll payment credentials via Visa Payment Passkeys — tokenized at enrollment, never passed in cleartext to agents. Users set spend parameters (merchant categories, caps, time windows) that the agent must operate within.

Current rollout: Hundreds of controlled live transactions confirmed December 2025. Visa "opened the door" globally in April 2026 with a pilot covering AWS, Aldar, Highnote, and others in the US, Asia Pacific, and Europe. Mainstream consumer adoption target: Holiday 2026.

This is live infrastructure with a developer spec, not a press release. But volume is pilot scale. The network tokens architecture that underlies the Visa Passkey credential is the same tokenization infrastructure used for mobile contactless today.

The network layer: Mastercard Agent Pay

Mastercard announced Agent Pay in April 2025 and confirmed Europe's first live end-to-end AI agent payment in March 2026 — Santander executing a transaction via Mastercard's framework.

Agentic Tokens: The key innovation. Where a standard card-on-file network token represents a card credential stored with one merchant, a Mastercard Agentic Token is issued per AI service. A single card can carry separate tokens for ChatGPT, Google Gemini, and Perplexity simultaneously. Each token is scoped at issuance — merchant categories, spending caps, time windows — and can be revoked independently. The agent never receives the card number.

Verifiable Intent: The consumer declares a high-level intent ("buy camping supplies for the weekend") before the agent acts. This intent is stored as a signed artifact on Mastercard's infrastructure. When the agent executes a transaction, the cart is checked against the declared intent. A luxury watch in the camping cart would be flagged or stepped up for authentication.

Know Your Agent (KYA): An agent registration/onboarding process analogous to KYC, using Web Bot Auth built on IETF RFC 9421 for cryptographic agent identity verification. Only registered agents receive Agentic Tokens.

Live rollout milestones: Citi and US Bank at launch (April 2025); PayPal (hundreds of millions of consumers in scope) added October 2025; Commonwealth Bank Australia and Westpac New Zealand in early 2026; Europe first live payment confirmed March 2026. The framework is rolling out issuer by issuer — coverage depends on your customers' banks.

The coordination layer: Google A2A and AP2

A2A (Agent2Agent Protocol): Announced April 2025, donated to the Linux Foundation June 2025, 150+ organizations and enterprise production use by its first anniversary. Defines how agents discover, authenticate with, and delegate tasks to other agents. PayPal is a launch partner.

AP2 (Agent Payments Protocol): Announced September 2025 as an extension to A2A adding payment-specific semantics — how agents pass payment credentials, confirm authorization, and handle receipts in agent-to-agent flows. Partners include Adyen, Mastercard, PayPal, Revolut, and Worldpay (60+ total). AP2 is in active partner development, not yet widely deployed as a standalone standard.

The relationship between the three protocols: MCP handles agent-to-API calls (one agent talking to a payment service); A2A handles agent-to-agent coordination (a purchasing agent delegating to a payment execution agent); AP2 adds the payment semantics to that agent-to-agent handoff. For complex agentic commerce workflows — a travel agent coordinating flights, hotels, and payments through separate sub-agents — the A2A + AP2 combination is the emerging standard.

The auth and security gap

The hardest problem in agent payments is authorization: proving an AI agent is acting on a specific human's explicit instruction, for a specific scope, at a specific time.

Visa and Mastercard have solved this at the network level through tokenized scoped credentials — the consumer authenticates once with biometric or Passkey at mandate setup, and subsequent agent transactions within scope proceed without step-up. This maps onto the existing MIT (merchant-initiated transaction) framework: pre-authorized by the consumer, executed autonomously within declared parameters.

The regulatory vacuum: PSD3 and PSR reached political agreement November 2025, published final text April 2026. Neither contains AI-agent-specific SCA provisions. The EU and UK frameworks for Strong Customer Authentication were designed around human-initiated transactions. Whether agent transactions qualify as MITs (SCA-exempt) or require a new category is unresolved in law, even though Visa and Mastercard have implemented the network-level mechanism.

Operators building agent payment integrations today are operating in a gap between what the card networks have shipped and what the regulators have addressed. The practical advice from legal analysis (Ashurst, Norton Rose): treat agent transactions as MITs where the consumer mandate covers the scope, document the mandate setup authentication, and monitor PSD3/PSR technical standards closely as they develop through 2027-2028.

Fraud signals for agent traffic: Traditional fraud detection relies on human behavioral signals — mouse movements, typing cadence, device fingerprints, session timing. Agent traffic generates none of these. AI scam volumes surged 1,210% in 2025 (Experian). Stripe's Agentic Commerce Suite explicitly notes traditional fraud tools are less effective for agent transactions and ships dedicated agentic fraud signals. Visa's Trusted Agent Protocol addresses a piece of this by verifying agent identity cryptographically, but the fraud model for agent traffic is still being built across the industry.

What agents can actually do in production today

The IMF's April 2026 analysis found AI agents succeed on approximately 50% of complex multi-step tasks in real environments. 8.4 million LLM call failures in early 2026 were rate-limit-related. Only 14% of enterprises have successfully scaled any AI agent to organization-wide use.

Confirmed in production:

- Checkout automation with live transactions: Visa (hundreds of controlled transactions, December 2025), Mastercard/Santander (Europe, March 2026), OpenAI Instant Checkout via Stripe ACP

- Refund processing automation: AI agents handling customer service refund flows at scale (Fini, Siena's Cognitive Reasoning Engine — documented 2M+ queries in production)

- Subscription management via Stripe toolkit: create/cancel subscriptions callable in production SaaS billing workflows

- Invoice and payment link generation: fully available via Stripe MCP and toolkit today

Known failure modes:

- Cascading errors: a bad tool selection early in a multi-step agent workflow can propagate to an irreversible payment with no human checkpoint

- Rate limit failures at volume: agent workflows that call Stripe or other payment APIs at high frequency hit rate limits that are not an issue for human-driven flows

- Liability ambiguity: when an agent initiates a wrong transaction, current law does not clearly assign responsibility between consumer, AI provider, and merchant

The operator decision

If you are a merchant or platform operator, the question is not whether to support agent-initiated transactions — that decision is being made by Visa, Mastercard, Stripe, and your customers' banks. The question is how to build safely.

For existing Stripe integrations: The MCP server and Agent Toolkit are available today. Start with restricted API keys scoped narrowly to the operations you want agents to access. Add logging at the API key level to distinguish agent-initiated from human-initiated transactions. Use Stripe's Agentic Fraud Protection (part of Agentic Commerce Suite) if you expose the ACP endpoint.

For authorization rates on agent traffic: The existing authorization optimization playbook applies, but agent transactions need separate monitoring. Auth rate behavior differs — no SCA step-up friction, but also no behavioral trust signals that issuers use for uplift.

For orchestration and multi-acquirer routing: Agent-initiated transactions change the routing calculus. MIT-exempt transactions may route differently than CIT transactions. Update routing rules to account for the new transaction category.

For PCI scope: Agent-to-API flows where a card number is never transmitted to the agent (Mastercard Agentic Tokens, Visa Passkey tokens, Stripe's Shared Payment Tokens) are designed to keep agents out of PCI scope. The PCI DSS 4.0 obligations that already apply to your checkout pages apply equally to any new agent-accessible flow — verify the data path before assuming agents are out of scope.

The agent payment stack is not coming. It arrived. The operators who understand the protocol stack, the network credential model, and the authorization gap will ship faster and with fewer compliance surprises than those treating it as a future problem.

Sources & methodology (10)

MCP released November 25, 2024; donated to Agentic AI Foundation (Linux Foundation) in December 2025

Checked:

97 million monthly MCP SDK downloads; 10,000+ public MCP servers (March 2026)

Checked:

Stripe MCP server at mcp.stripe.com supports ~25 tools; OAuth-authenticated; production as of Stripe Sessions April 2026

Checked:

Stripe Agentic Commerce Suite announced December 2025 — ACP endpoint, Shared Payment Tokens, Agentic Fraud Protection

Checked:

Visa Intelligent Commerce announced April 30, 2025; Trusted Agent Protocol (TAP) launched October 2025

Checked:

Mastercard Agent Pay announced April 2025; Santander + Mastercard completed Europe's first live end-to-end AI agent payment March 2026

Checked:

AI agents succeed on only ~50% of complex multi-step tasks in real environments; 8.4M rate-limit failures in early 2026

Checked:

PSD3/PSR final text published April 2026 contains no AI-agent-specific SCA provisions

Checked:

AI scam volumes surged 1,210% in 2025; Experian names agentic AI as top 2026 fraud threat

Checked:

Google AP2 (Agent Payments Protocol) announced September 2025 with 60+ partners including Adyen, Mastercard, PayPal, Revolut

Checked:

Source types explained in our Methodology.