SEPA Return and Reject Codes: The R-Transaction Reference

Every SEPA R-transaction reason code — reject, return, refund, reversal, refusal, recall — across SCT, SCT Inst, and SDD, with what each means for operators.

Six SEPA R-transaction types: Reject, Return, Refund, Reversal, Refusal, Recall. SDD Core: 8-week authorized / 13-month unauthorized refund. SDD B2B: no refund; 3-day irrevocability. SCT Recall 10 days (FRAD 13 months); RFRO 13 months. MS03 masks AC04/AM04 by data-protection law.

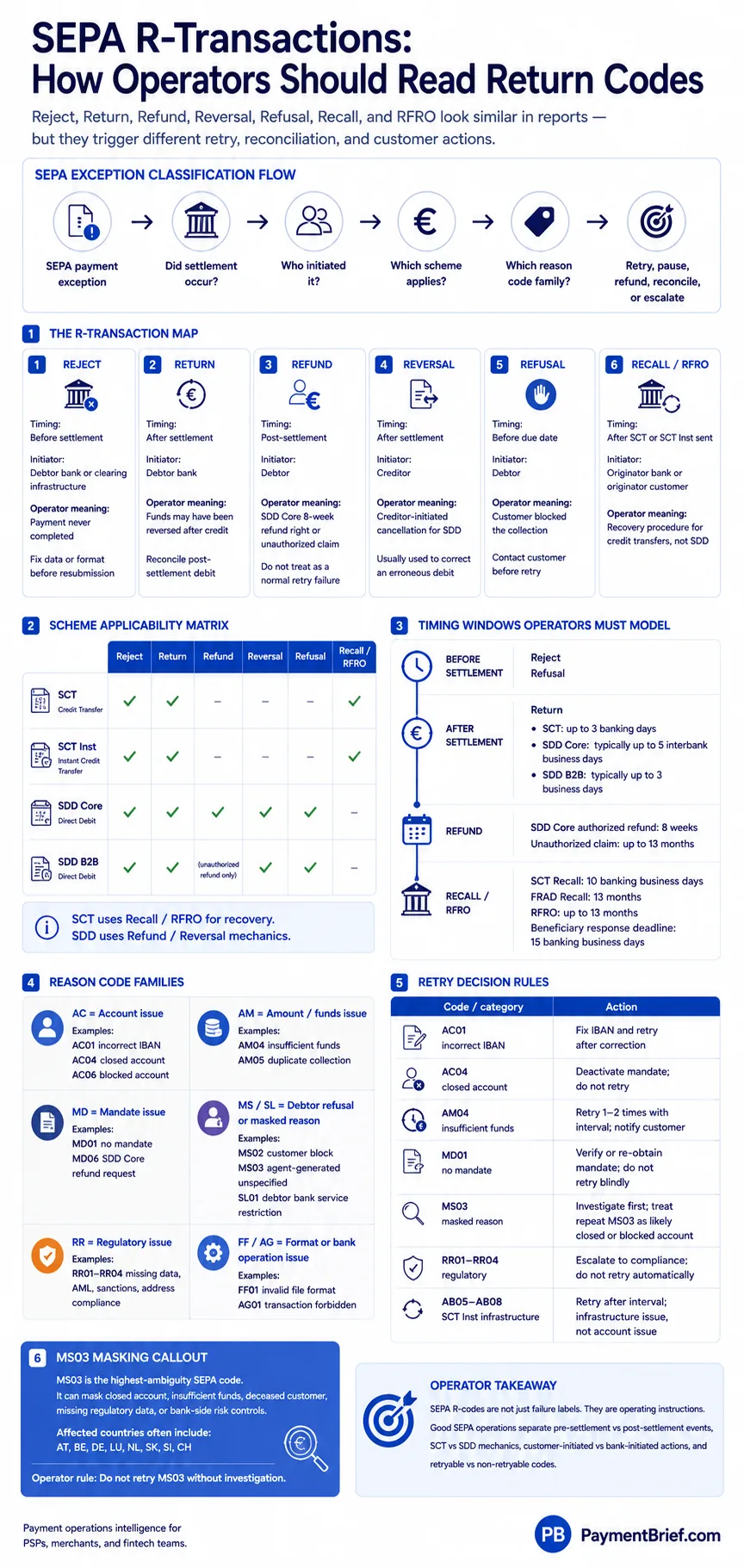

SEPA R-transactions are any payment that does not complete as initiated — covering six distinct types: Reject (pre-settlement bank refusal), Return (post-settlement bank reversal), Refund (debtor exercises refund right), Reversal (creditor-initiated post-settlement cancellation, SDD only), Refusal (debtor blocks before settlement), and Recall/RFRO (recovery procedures for sent SCT). Each type has a different initiating party, timing window, and set of ISO 20022 reason codes. SDD Core allows an 8-week no-questions-asked refund and a 13-month window for unauthorized claims. SDD B2B has no consumer refund right and is typically treated as irrevocable after approximately three business days following settlement (verify exact handling with your PSP or bank).

A reference map of every material SEPA R-transaction type and reason code, covering all four schemes — SCT, SCT Inst, SDD Core, SDD B2B — with scheme applicability, timing windows, and operator action guidance. For background on how the four SEPA schemes work — mandate lifecycle, submission deadlines, SCT Inst mandatory rollout — see SEPA Credit Transfer, Instant, and Direct Debit: Operator Guide. For how direct debit compares to ACH, Bacs, and eGIRO see Direct Debit Payments Explained.

How operators should read SEPA return codes — the six R-transaction types, which schemes each applies to, the key reason codes, and the timing windows that govern recovery.

The six R-transaction types

R-transactions in SEPA are not a single class of failure. The six types differ in who initiates them, whether settlement has occurred, and what the creditor can do in response. Treating them as interchangeable in reconciliation or retry logic generates compliance violations and customer complaints.

| Type | Initiator | Timing | Settlement occurred? | ISO 20022 message |

|---|---|---|---|---|

| Reject | Debtor bank or clearing infrastructure | Before settlement | No | pacs.002 |

| Refusal | Debtor (via their bank) | Up to D-1 before due date | No | pacs.002 |

| Return | Debtor bank | After settlement (SCT: 3 banking days; SDD Core: typically 5 days; SDD B2B: typically 3 days) | Yes | pacs.004 |

| Refund | Debtor (via their bank) | Up to 8 weeks post-settlement (SDD Core) | Yes | pacs.004 |

| Reversal | Creditor (via their bank) | After settlement, typically within 5 business days | Yes (SDD only) | pacs.007 |

| Recall | Originator bank | Up to 10 banking business days (FRAD: 13 months) | Yes (SCT/SCT Inst) | camt.056 |

| RFRO | Originator (customer-initiated, via originator bank) | Up to 13 months | Yes (SCT/SCT Inst) | camt.056 |

Reject vs Return: Both result in no net credit to the creditor, but their cause and operational response differ. A Reject stops the payment before funds move; no revenue is at risk. A Return reverses funds already credited — the creditor loses settled revenue and must reconcile a post-settlement debit.

Refusal vs Reject: A Refusal is debtor-instructed — the customer has told their bank not to honor this specific collection. A Reject is bank-side, often technical. A pattern of Refusals on the same mandate is a customer relationship signal; a pattern of Rejects on the same creditor is a data quality signal.

Recall and RFRO apply to SCT and SCT Inst only. They are not R-transaction types for SDD. See the Recall and RFRO section below for the two procedures and their reason codes.

Reversal applies to SDD Core and SDD B2B only. It is the creditor-initiated post-settlement cancellation of a direct debit collection. The SCT scheme does not define a Reversal R-transaction; the equivalent recovery mechanism for SCT is the Recall/RFRO procedure.

Scheme applicability matrix

| R-type | SCT | SCT Inst | SDD Core | SDD B2B |

|---|---|---|---|---|

| Reject | Yes | Yes | Yes | Yes |

| Refusal | No | No | Yes | Yes |

| Return | Yes (≤3 days) | Yes (post-settlement; rejects within 10 seconds) | Yes (≤5 days) | Yes (≤3 days) |

| Refund (8-week) | No | No | Yes | No |

| Refund (13-month unauthorized) | No | No | Yes | Yes (unauthorized only) |

| Reversal | No | No | Yes | Yes |

| Recall (bank-initiated) | Yes | Yes | No | No |

| RFRO (customer-initiated) | Yes | Yes | No | No |

R-transaction timing and deadlines

Source: EPC SDD Core Rulebook 2025 v1.1 (EPC016-06), SDD B2B Rulebook 2025 v1.1 (EPC222-07), and EPC Clarification Paper EPC131-17 v3.1 (April 2025).

| R-type | SDD Core | SDD B2B | SCT | SCT Inst |

|---|---|---|---|---|

| Reject | Pre-settlement; same-day as collection | Pre-settlement; same-day | Pre-settlement; same-day | Seconds; hard 10-second limit |

| Refusal | Up to D-1 (one banking day before due date) | Up to D-1 | N/A | N/A |

| Return | Up to 5 interbank business days post-settlement | Up to 3 business days post-settlement | Up to 3 banking business days post-settlement | Post-settlement returns follow a longer window; negative confirmations (rejects) happen within the 10-second execution window |

| Refund (authorized) | Up to 8 weeks post-settlement | Not available | N/A | N/A |

| Refund (unauthorized) | Up to 13 months post-settlement | Up to 13 months post-settlement | N/A | N/A |

| Reversal | After settlement, within 5 business days (creditor-initiated) | After settlement, within 5 business days | N/A (SCT has no Reversal; use Recall/RFRO) | N/A |

| Recall (bank-initiated) | N/A | N/A | 10 banking business days (FRAD: 13 months) | 10 banking business days (FRAD: 13 months) |

| RFRO (customer-initiated) | N/A | N/A | Up to 13 months | Up to 13 months |

SDD B2B irrevocability. Under the SDD B2B scheme rules, an authorized B2B direct debit is typically treated as irrevocable once approximately three business days pass after the debit date without a return. The debtor's bank cannot initiate a refund on the debtor's behalf. This is the primary operational reason B2B billing operators prefer SDD B2B over SDD Core for invoice collection: the 8-week uncertainty window does not exist.

SCT recall and RFRO response obligation. Once a Recall or RFRO (camt.056) is received, the beneficiary bank has 15 banking business days to respond. If no response arrives within that window, the lack of response constitutes a breach of the SCT rulebook. The Recall and RFRO section below covers both procedures and their reason codes.

Reason code reference: SDD

All codes below are ISO 20022 External Return Reason codes as published in the EPC guidance documents EPC173-14 v8.0 (SDD, November 2024). The v8.0 update added structured address requirements to RR02 and RR03; all other codes are stable across v6.0–v8.0.

Account codes (AC)

| Code | Name | Typical cause | SDD Core | SDD B2B | R-types |

|---|---|---|---|---|---|

| AC01 | Incorrect account number | IBAN format invalid or account does not exist | Yes | Yes | Reject, Return |

| AC04 | Closed account number | Debtor's account has been closed | Yes | Yes | Reject, Return |

| AC06 | Blocked account | Account frozen — debtor action, bankruptcy, or bank restriction | Yes | Yes | Reject, Return |

| AC13 | Debtor account type invalid | Account type does not permit direct debits (e.g., savings account) | Yes | Yes | Reject |

AC04 note: In several SEPA countries (Austria, Belgium, Germany, Luxembourg, Netherlands, Slovakia, Slovenia, Switzerland), data protection law prohibits the debtor bank from disclosing that an account is closed. In these jurisdictions, AC04 is replaced by MS03. See the MS03 section below.

Amount and funds codes (AM)

| Code | Name | Typical cause | SDD Core | SDD B2B | R-types |

|---|---|---|---|---|---|

| AM04 | Insufficient funds | Account balance below collection amount | Yes | Yes | Return |

| AM05 | Duplicate collection | Same debit submitted more than once | Yes | Yes | Reject, Return |

AM04 note: Same data protection masking applies as AC04 in the listed jurisdictions — AM04 may appear as MS03.

Mandate codes (MD)

| Code | Name | Typical cause | SDD Core | SDD B2B | R-types |

|---|---|---|---|---|---|

| MD01 | No mandate | No valid mandate on file; mandate cancelled; sequence type mismatch | Yes | Yes | Reject, Return |

| MD02 | Mandate data missing or incorrect | Mandatory mandate fields absent or malformed | Yes | Yes | Reject |

| MD06 | Refund request by end customer | Debtor exercises 8-week authorized refund right | Yes | No | Refund |

| MD07 | End customer deceased | Account holder has died | Yes | Yes | Reject, Return |

MD01 is the highest-signal mandate failure code. It means the debtor's bank checked and could not match the mandate data in the collection message to a valid registered mandate. For SDD B2B, where mandates are pre-registered at the debtor's bank, MD01 is particularly definitive — the bank explicitly verified and rejected.

MD06 is SDD Core only. It appears on the pacs.004 refund message and carries the 8-week window. There is no MD06 equivalent in SDD B2B. If a B2B debtor wants to contest a collection, they must do so as an unauthorized claim (no valid mandate) via a different process.

Agent and format codes (AG / FF)

| Code | Name | Typical cause | SDD Core | SDD B2B | R-types |

|---|---|---|---|---|---|

| AG01 | Transaction forbidden | Account does not accept direct debits (regulatory restriction or account type) | Yes | Yes | Reject, Return |

| AG02 | Invalid bank operation code | Message structure incorrect; local instrument code invalid | Yes | Yes | Reject |

| FF01 | Invalid file format | General format error; message does not conform to ISO 20022 schema | Yes | Yes | Reject |

| FF05 | Local instrument code invalid | LocalInstrument field (CORE or B2B) does not match account capabilities | Yes | Yes | Reject |

BE05 (incorrect Creditor Identifier) also appears in the EPC guidance as an agent-category reject, but is listed under party identification rather than the AG/FF grouping in ISO 20022 external code sets. It means the Creditor ID in the message does not match a registered creditor — a common failure in new SDD program setup.

Regulatory codes (RR)

| Code | Name | Typical cause | SDD Core | SDD B2B | R-types |

|---|---|---|---|---|---|

| RR01 | Missing debtor account or identification | Regulatory requirement for debtor account ID not met | Yes | Yes | Reject, Return |

| RR02 | Missing debtor name or address | Name or address required for regulatory compliance is absent or invalid (updated v8.0: includes structured address format) | Yes | Yes | Reject, Return |

| RR03 | Missing creditor name or address | Creditor name or address required for regulatory compliance is absent or invalid (updated v8.0: includes structured address format) | Yes | Yes | Reject, Return |

| RR04 | Regulatory reason | Sanctions screening, AML block, or other regulatory hold — reason not further specified | Yes | Yes | Reject, Return |

RR01–RR04 are returned immediately where possible. They indicate the collection cannot proceed due to compliance requirements rather than debtor account issues. RR04 in particular may reflect a sanctions hit or an AML flag on either side of the transaction.

RR02 and RR03 in v8.0: The November 2024 update to EPC173-14 extended these codes to cover structured address format violations. From October 2025, the 2025 rulebooks require hybrid or structured address formats — unstructured address format phases out by November 2026. Collections with non-compliant address formats may now return RR02 or RR03 rather than AG02.

Debtor refusal and unspecified codes (MS / SL)

| Code | Name | Typical cause | SDD Core | SDD B2B | R-types |

|---|---|---|---|---|---|

| MS02 | Not specified — customer-generated | Debtor has blocked this collection (no further reason given) | Yes | Yes | Refusal, Return |

| MS03 | Not specified — agent-generated | Bank withholds reason (data protection, risk controls, or catch-all) | Yes | Yes | Reject, Return |

| SL01 | Specific debtor bank service | Creditor not on debtor's whitelist; collection exceeds debtor's configured limit | Yes | Yes | Reject, Return |

The MS03 masking point

MS03 is the single highest-ambiguity code in SEPA. It means the bank has processed the R-transaction but is not disclosing the reason. There are three distinct causes:

-

Data protection substitution. The EPC guidance (EPC173-14, consistent from v4.0 through v8.0) states that MS03 must be used when national legislation does not permit disclosure of AC04 (closed account), AM04 (insufficient funds), MD07 (deceased), RR01, RR02, RR03, or RR04. The countries identified in EPC guidance as applying these restrictions are Austria, Belgium, Germany, Luxembourg, the Netherlands, Slovakia, Slovenia, and Switzerland. In practice, when you receive MS03 from a debtor bank in these countries, it is most commonly either AC04 or AM04.

-

Bank-side risk control. Some banks use MS03 when their internal fraud or risk scoring has flagged the transaction — beyond what any specific code covers.

-

Genuine unspecified error. A catch-all for edge cases the bank cannot categorize under a more specific code.

Operational treatment: Do not retry MS03 without investigation. Treat it as you would AC04 on first occurrence — check with the customer whether the account is active, and update mandate status if the customer confirms account closure. On repeat MS03 from the same mandate without customer contact, treat as a likely closed/blocked account and pause collections.

Reason code reference: SCT and SCT Inst

SCT and SCT Inst share most reason codes, but SCT Inst adds several codes specific to the 10-second settlement window and the instant scheme infrastructure. The EPC guidance document for SCT R-transactions is EPC135-18 v6.0 (November 2024); for SCT Inst it is EPC059-18 v6.0 (November 2024).

Account and format codes

| Code | Name | SCT | SCT Inst | R-types |

|---|---|---|---|---|

| AC01 | Incorrect account number | Yes | Yes | Reject, Return |

| AC03 | Wrong IBAN (creditor) | Yes | Yes | Return |

| AC04 | Closed account | Yes | Yes | Return |

| AC06 | Blocked account | Yes | Yes | Return |

| FF01 | Invalid file format | Yes | Yes | Reject |

| AM04 | Insufficient funds | Yes | Yes | Return |

| AM05 | Duplicate payment | Yes | Yes | Reject, Return |

| RC01 | Incorrect BIC | Yes | Yes | Return |

| CNOR | Creditor bank not registered | Yes | Yes | Return |

| DNOR | Debtor bank not registered | Yes | Yes | Return |

SCT Inst-specific codes

| Code | Name | Cause | R-types |

|---|---|---|---|

| AG09 | Payment not received by creditor agent | Creditor bank did not receive within 10-second window | Return |

| AG10 | Agent suspended from instant scheme | Bank excluded from SCT Inst network | Return |

| AG11 | Creditor agent suspended | Beneficiary bank suspended | Return |

| AM02 | Amount exceeds agreed limit | Transaction exceeds a limit set by the debtor PSP or agreed between PSPs (the 2025 SCT Inst rulebook removed the former €100,000 scheme-level cap; PSPs now set their own limits, which under the EU IPR cannot be lower than their SCT limits) | Reject |

| AB05 | Timeout at creditor agent | Creditor bank failed to respond within 10 seconds | Return |

| AB06 | Timeout at instructed agent | Intermediate agent timeout | Return |

| AB07 | Agent offline | Participating bank unreachable | Return |

| AB08 | Creditor agent offline | Beneficiary bank system down | Return |

SCT Inst rejects and returns come back within seconds under normal conditions — the 10-second settlement deadline means there is no "next day" return for timing reasons. The AB and AG codes above are infrastructure codes; they indicate a bank or scheme connectivity issue rather than an account issue. Retry after a brief interval is appropriate for AB/AG codes. For the operational handling — what to do at each failure class, pacs.002 status mechanics, and escalation checklists — see the SCT Inst rejection and timeout runbook.

Regulatory codes (shared SCT/SDD)

RR01–RR04 apply to SCT and SCT Inst with the same meanings as SDD. RR02 and RR03 were updated in v6.0 of the SCT guidance (November 2024) to include structured address format requirements, aligned with the 2025 rulebook address change described above.

SCT Recall and RFRO: two recovery procedures

Recovery of a sent SCT or SCT Inst is handled through two distinct procedures, both using camt.056 (Cancellation Request) and camt.029 (Resolution of Investigation). They differ in who initiates them, which reason codes they use, and how long the window is.

Beneficiary response deadline (both procedures): 15 banking business days from receipt of the camt.056. Non-response within this window constitutes a rulebook breach.

Recall (bank-initiated)

The Recall procedure is initiated by the originator bank — not the customer directly. It covers three reason codes:

Initiation window: 10 banking business days from the execution date; FRAD extends to 13 months.

| Recall reason code | Name | Notes |

|---|---|---|

| DUPL | Duplicate payment | Two identical pacs.008 messages submitted; originator bank initiates recovery of one |

| TECH | Technical problem | Processing error on the originator side; bank-initiated, not a customer request |

| FRAD | Fraudulent origin | Suspected fraud; 13-month window; beneficiary bank assesses and decides whether to return |

Request for Recall by the Originator (RFRO)

The RFRO is initiated by the customer via their originator bank. It covers situations where the customer sent the payment in error — wrong beneficiary IBAN, wrong amount, or a duplicate the customer identified. The originator bank passes the customer's request to the beneficiary bank via camt.056.

Initiation window: Up to 13 months from the execution date for all RFRO reasons.

| RFRO reason code | Name | Notes |

|---|---|---|

| CUST | Customer request | Customer asks for recovery (wrong beneficiary, duplicate identified by customer); beneficiary consent required — beneficiary can legitimately decline |

| AM09 | Wrong amount | Customer identifies incorrect amount was sent |

| AC03 | Wrong creditor IBAN | Customer identifies incorrect IBAN was used |

RFRO vs Recall: The 13-month RFRO window is available for all customer-initiated reasons — not just FRAD. The beneficiary can decline an RFRO (unlike FRAD recall, where refusal carries regulatory and legal risk). For CUST/AM09/AC03, the beneficiary can legitimately refuse if funds have already been applied.

Responses to both Recall and RFRO

Positive response (FOCR): If the beneficiary bank agrees, they send the funds back via pacs.004 with reason code FOCR (Return Following Cancellation Request). FOCR is the only valid reason code for a positive response.

Negative response codes (camt.029): If the beneficiary cannot or will not comply, they send a camt.029 with one of:

- NOOR — transaction not received (funds never arrived)

- ARDT — already returned (funds were already reversed)

- LEGL — legal decision prevents return

- AC04 — account closed (funds cannot be returned from a closed account)

Operator action table

For each code or category, the action required differs. This table covers the most common codes operators encounter in production.

| Code / Category | Likely cause | Operator action | Retry? |

|---|---|---|---|

| AC01 (incorrect IBAN) | Mandate data error; transposition in IBAN | Validate IBAN with IBAN check tool; contact customer for correction | Yes, after correction |

| AC04 (closed account) | Account closed since mandate was created | Deactivate mandate; contact customer for new account | No — do not retry on closed account |

| AC06 (blocked account) | Account frozen (debtor action, legal order) | Pause collections on this mandate; contact customer | No until customer confirms unblocked |

| AM04 (insufficient funds) | Insufficient balance at collection time | Retry per your policy; notify customer; consider payment plan | Yes (1–2 retries with interval) |

| MD01 (no mandate) | Mandate cancelled, sequence mismatch, or B2B mandate not pre-registered | Verify mandate status; re-obtain mandate if cancelled | No — re-mandate required |

| MD06 (refund request) | Customer exercised 8-week SDD Core right | Accept — no contest right; investigate if recurrent; review mandate validity | No |

| MS02 (customer block) | Debtor instructed their bank not to pay | Contact customer; investigate reason before any retry | No |

| MS03 (unspecified, agent) | Closed account / insufficient funds (masked) or bank-side restriction | Treat as AC04 on first occurrence; contact customer | No until verified |

| FF01 (format error) | Message schema error; invalid IBAN or mandate reference format | Fix message data; re-validate before resubmission | Yes, after fix |

| RR01–RR04 (regulatory) | Sanctions, AML, KYC, address compliance failure | Do not retry without compliance review; escalate internally | No — compliance review required |

| AG01 (transaction forbidden) | Account type restriction or debtor bank policy | Contact debtor bank if persistent; consider alternative payment method | No |

| SL01 (service restriction) | Creditor not on debtor whitelist or amount limit exceeded | Contact customer to update whitelist; check B2B mandate limits | No until customer action |

| DUPL recall (SCT) | Duplicate submission (Recall, bank-initiated) | Confirm one of the two payments is recovered; reconcile | N/A |

| FRAD recall (SCT) | Fraud-originated transfer (Recall, bank-initiated, 13-month window) | Cooperate immediately; legal obligation to return if funds available | N/A |

| CUST/AM09/AC03 RFRO (SCT) | Customer-initiated recall (wrong amount, wrong IBAN, or customer request) | Assess and respond within 15 banking business days; you may legitimately decline if funds already applied | N/A |

| AB05–AB08 (SCT Inst infrastructure) | Bank or network timeout | Retry after interval (infrastructure-level, not account-level) | Yes |

Common failure patterns and reduction strategies

IBAN validation on mandate capture

AC01 (incorrect IBAN) and AC04 (closed account as proxy) are the most preventable codes. An IBAN check at mandate capture — verifying the check digit and country-format validity — eliminates the majority of AC01 failures before the first collection. Most PSPs (Stripe, GoCardless, Adyen) run IBAN validation automatically; direct integrations must implement it explicitly.

From October 2025, the EU's Verification of Payee (VoP) requirement mandates that PSPs check IBAN-to-name matches before executing outbound SCT and SCT Inst. This also reduces first-collection failures where customers accidentally provide an account belonging to someone else. See EU Instant Payments Regulation: The Compliance Timeline for VoP implementation details.

Mandate sequence hygiene

MD01 (no mandate) on recurring SDD collections is almost always a lifecycle management failure. The three common causes: the mandate was cancelled by the customer directly via their bank but the creditor's system was not notified; the SequenceType field was set incorrectly (FRST vs RCUR vs FNAL); or for SDD B2B, the mandate was not pre-registered at the debtor's bank before the first collection attempt.

Reconciling MD01 returns to the specific mandate reference and sequence type in the original message identifies which failure mode applies. A pattern of MD01 at FRST (first collection) typically indicates the pre-registration step was skipped for B2B, or the mandate was not stored correctly. A pattern of MD01 at RCUR typically indicates the customer cancelled at their bank.

Retry strategy for AM04 and MS03

AM04 (insufficient funds) supports retry — but scheme rules and good practice both impose limits. Retry once 3–5 banking days after the initial failure, typically mid-month for subscription billing aligned to payroll cycles. A second AM04 on the same collection period should trigger customer notification rather than another automated retry. Never retry the same collection more than twice without customer engagement; repeated attempts on a blocked or closed account generate scheme violations.

MS03 requires classification before retry. If the debtor is reachable and confirms the account is active, a single retry is reasonable. If the debtor is unreachable or if prior collections on the same mandate have failed with AM04 or AC04, treat MS03 as a likely closed account and pause rather than retry.

SDD Core refund window management

The 8-week SDD Core refund window is not a dispute mechanism — it requires no justification from the debtor. For subscription operators, this creates a two-month exposure window on every collection. Revenue recognition from SDD Core should account for this; finance models that treat SDD Core settlements as final on D+1 overstate confirmed revenue by the amount of expected refunds.

Practical mitigation: send clear pre-collection notifications (meeting the 14-day rulebook requirement or the shorter agreed period), ensure cancellation processes work cleanly so customers who want to cancel don't need to exercise the refund right, and track MD06 frequency as a customer satisfaction metric alongside chargeback rates.

B2B mandate pre-registration

The SDD B2B sequence is: (1) obtain mandate, (2) send mandate data to debtor's bank for registration, (3) wait for bank confirmation, (4) initiate first collection. Skipping step 2 and going directly to collection generates MD01 on B2B — the debtor's bank checks registered mandates and finds none. The pre-registration lag varies by bank but is typically 1–3 business days. Build this into the onboarding flow rather than treating it as optional.

For recurring payments across rails

SEPA R-transactions interact with broader subscription-billing failure management. For the cross-rail comparison of how retry logic, mandate management, and return codes differ across ACH, Bacs, SEPA SDD, and eGIRO, see Recurring Payments: Rails Compared.

Scope note

- Primary sources: EPC scheme rulebooks (SCT, SCT Inst, SDD Core, SDD B2B) and reason-code guidance, plus the ISO 20022 external code sets. Full citations are listed under Sources below.

- Rulebook-backed: the six R-transaction types, scheme applicability, reason-code meanings, the three-banking-day SCT return window, and the Recall (bank-initiated) versus RFRO (customer-initiated) split. The SCT Inst €100,000 scheme cap was removed in the 2025 rulebook alongside the EU Instant Payments Regulation.

- Data-protection masking (MS03): the substitution of MS03 for AC04, AM04, MD07, and RR01–RR04, and the affected country list, come from EPC SDD reason-code guidance and are consistent across recent rulebook versions.

- Operator/PSP-sourced: the SDD B2B three-business-day return window and the five-business-day Reversal window are drawn from operator and PSP guides where the EPC rulebook PDFs were inaccessible — treat these two figures as indicative.

- Verify with your bank or PSP: exact deadlines, CSM cut-off times, and code applicability vary by rulebook version, bank handling, and PSP implementation.

Related references

- SEPA Credit Transfer, Instant, and Direct Debit: Operator Guide — mandate lifecycle, scheme selection, and SCT Inst mandatory rollout.

- Direct Debit Payments Explained: ACH, SEPA, Bacs, eGIRO — cross-rail return code comparison and mandate mechanics.

- EU Instant Payments Regulation: The Compliance Timeline — VoP implementation, SCT Inst mandate, and address format obligations.

- Recurring Payments: Rails Compared — retry strategy, return window modeling, and subscription billing rail selection.

For term definitions — SEPA, IBAN, direct debit, recurring payment — see the Payments Glossary.

Sources & methodology (13)

EPC guidance on R-transaction reason codes for SDD — version 8.0 published November 2024, applies to 2025 SDD rulebooks in force from October 5, 2025

Checked:

EPC guidance on R-transaction reason codes for SCT — version 6.0 published November 2024, applies to 2025 SCT rulebooks in force from October 5, 2025

Checked:

EPC guidance on R-transaction reason codes for SCT Inst — version 6.0, November 2024

Checked:

SDD Core 2025 rulebook v1.1 — in force October 5, 2025; no changes to core business rules vs prior version

Checked:

SDD B2B 2025 rulebook v1.1 — in force October 5, 2025; no consumer refund right, 3-business-day technical return window

Checked:

MS03 is to be used when national legislation (e.g. data protection law) does not allow the use of AC04, AM04, MD07, RR01, RR02, RR03, and RR04; applies in AT, BE, DE, LU, NL, SK, SI, CH

EPC guidance directly states MS03 substitutes enumerated codes where national law blocks disclosure; country list consistent across v4.0–v8.0

Checked:

SCT Recall (bank-initiated) must be initiated within 10 banking business days; FRAD recalls permitted up to 13 months. RFRO (Request for Recall by Originator, customer-initiated) allowed up to 13 months for all reasons (wrong IBAN, wrong amount, CUST). Beneficiary bank has 15 banking business days to respond to either procedure.

RFRO covers CUST/AM09/AC03; Recall covers DUPL/TECH/FRAD. Both use camt.056/camt.029. PDF blocked direct access; fact confirmed via EPC document library search results and Treezor API documentation citing EPC131-17.

Checked:

SCT Return window is 3 banking business days after settlement date (not 5); beneficiary bank must return via pacs.004 within D+3

SCT Rulebook specifies 3 banking business days; confirmed by multiple secondary sources quoting EPC125-05. The 5-day figure in the original article was incorrect.

Checked:

SCT Inst scheme maximum amount of €100,000 removed in 2025 rulebook; no EPC-level cap; PSPs set their own limits subject to EU IPR constraint (SCT Inst limits cannot be lower than SCT limits)

Confirmed by multiple sources including Mambu EPC 2025 SEPA Rulebook Updates. Applies from October 5, 2025.

Checked:

ISO 20022 External Return Reason codes — canonical definitions for AC01, AC04, AM04, MD01, MD06, MS03, RR01–RR04, and others

Checked:

SDD B2B payment deemed final three business days after debit date; payer not entitled to refund for authorized transaction

Checked:

R-transaction type definitions and timing: Reject pre-settlement, Return post-settlement, Refusal D-1 before due date, Reversal creditor-initiated post-settlement

Checked:

GoCardless SEPA Direct Debit failure message types and return codes

Checked:

Source types explained in our Methodology.