Saudi Arabia's Payment Stack: Mada, SARIE, and the Vision 2030 Infrastructure

How payments work in Saudi Arabia for operators: Mada debit (95%+ of cards), SARIE instant transfers, STC Pay — and the SAMA licensing or local-acquirer path.

Mada dominates Saudi domestic card transactions; e-payments hit 79% of retail in 2024 (SAMA); STC Pay has 12M Saudi users — SAMA licensing and mandatory Mada acceptance mean foreign operators need a licensed local acquirer like HyperPay or Checkout.com.

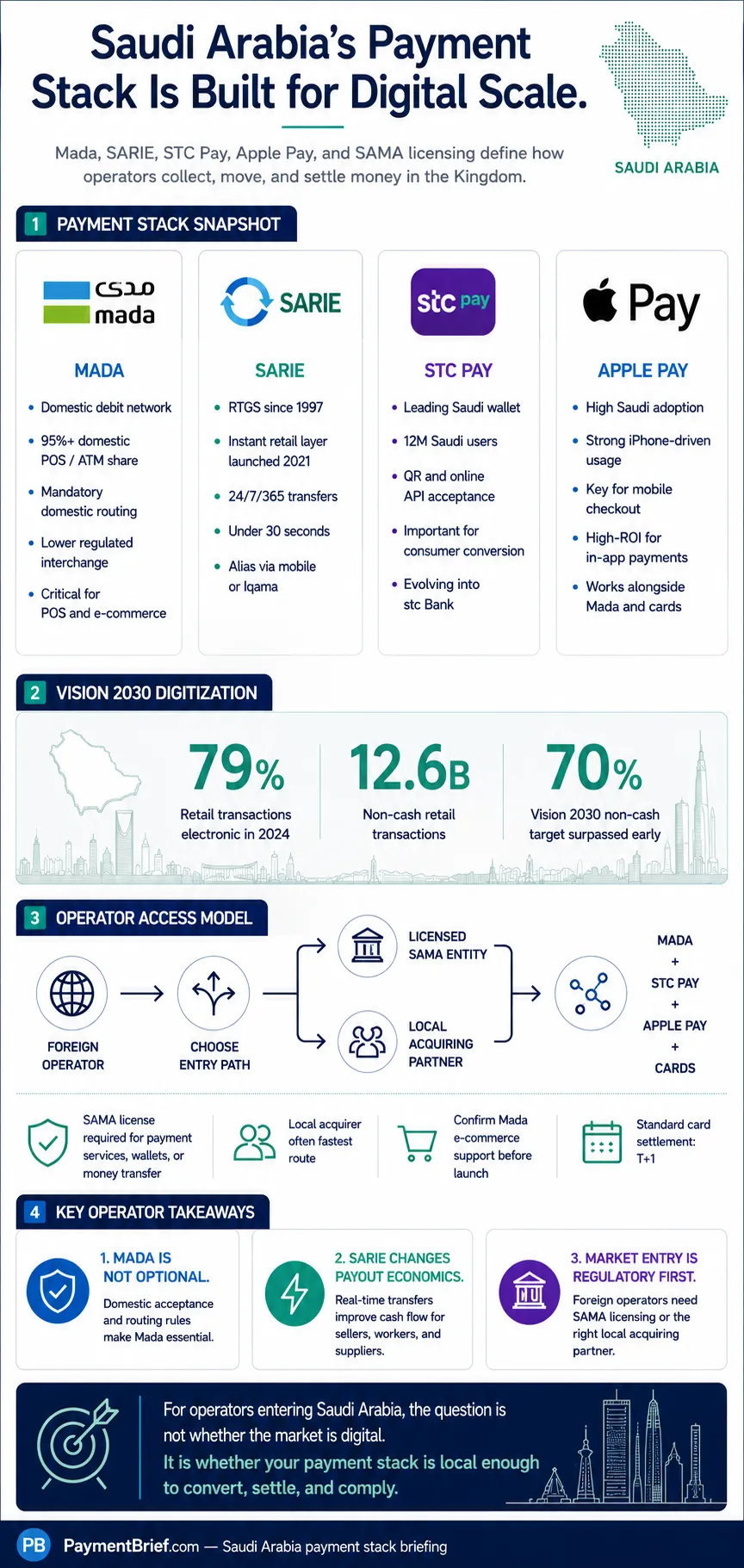

Saudi Arabia has executed one of the most deliberate payment infrastructure modernizations of any Gulf state. The Saudi Arabian Monetary Authority (SAMA) — the central bank — set a target of 70% non-cash transactions by 2025 as part of the Vision 2030 economic diversification program. Saudi Arabia surpassed this target ahead of schedule: electronic payments accounted for 79% of all retail transactions in 2024, up from 70% in 2023, with 12.6 billion non-cash retail transactions (SAMA, April 2025). The infrastructure built to achieve this shift — Mada for domestic card payments, SARIE for real-time interbank transfer, and a regulatory framework that mandates acceptance of these networks — is the operating environment every foreign operator serving the Saudi market must understand.

Mada: The Domestic Debit Network

Mada is Saudi Arabia's national domestic debit and prepaid card network, operated by Saudi Payments (formerly part of SAMA, now a subsidiary). Every Saudi bank issues Mada-branded debit cards; it is the most widely held payment instrument in the Kingdom. Mada processes approximately 95%+ of domestic point-of-sale and ATM transactions — a dominance level that makes it effectively a monopoly on domestic debit.

The Mada network operates as a four-party scheme similar to Visa and Mastercard, with Saudi Payments setting interchange rates and scheme rules. Most Saudi-issued cards are co-badged: Mada + Visa, or Mada + Mastercard. For domestic transactions, SAMA regulations require that the Mada network be used when available — merchants cannot route away from Mada to the international scheme for domestic Saudi card transactions. This is a least-cost routing mandate that benefits Saudi merchants (Mada interchange is regulated and lower than international scheme rates) and builds transaction volume on the domestic network.

Mada interchange: SAMA has regulated Mada interchange at low levels relative to international card networks. Current Mada interchange for debit transactions is approximately 0.5% or flat fee structures for certain merchant categories. This is meaningfully below Visa/Mastercard consumer debit interchange in comparable markets, making Mada acceptance economically attractive for merchants.

Mada for e-commerce: Mada launched an e-commerce variant — Mada Pay for online — that enables Mada-branded card transactions for card-not-present purchases. Prior to Mada Pay, many Saudi consumers with Mada-only cards (without an international scheme co-badge) could not make online purchases. Mada Pay's rollout expanded the addressable market for Saudi e-commerce. Acquirers operating in Saudi Arabia support Mada Pay; international operators must confirm Mada e-commerce acceptance with their acquiring partner.

Mada acceptance mandates: SAMA requires merchants above certain revenue thresholds in Saudi Arabia to accept Mada. This is a compliance requirement, not just a commercial consideration — and it is enforced. Foreign operators with physical presence in Saudi Arabia must ensure their point-of-sale infrastructure accepts Mada.

SARIE: 1997 RTGS, 2021 Instant Layer

SARIE — the Saudi Arabian Riyal Interbank Express — has been the Kingdom's RTGS rail since 1997. What launched in 2021 is the instant payment service ("sarie") built on top of it: a 24/7 real-time retail layer operated by Saudi Payments. Limits, identifiers (Alias via mobile or Iqama), and corporate access live on this newer instant layer; the underlying RTGS continues to handle high-value interbank settlement.

Key parameters of the instant layer:

- Speed: Real-time, under 30 seconds

- Availability: 24/7/365

- Transaction limit: SAR 300,000 per transaction (~$80,000 USD) for standard retail transfers (varies by channel and bank)

- Participants: All licensed Saudi commercial banks

SARIE is the underlying rail for Saudi Arabia's Alias payment system — transfers can be initiated using a mobile phone number or national ID (Iqama) as the beneficiary identifier, rather than requiring a bank account number. This reduces payment initiation friction significantly and has accelerated P2P transfer adoption.

SARIE for businesses: The SARIE network supports corporate payment initiation via bank API, enabling businesses to initiate bulk payroll, supplier payments, and B2B transfers. For operators disbursing to Saudi recipients (marketplace sellers, gig workers, insurance payouts), SARIE real-time bank transfer is the standard mechanism.

SARIE vs International Wire: Prior to SARIE's real-time capability, corporate payments within Saudi Arabia used the older batch SARIE system with business-hours settlement. The real-time upgrade changes cash flow dynamics for businesses with time-sensitive supplier payment obligations or seller payouts. International wires in and out of Saudi Arabia continue to flow through SWIFT, though Saudi banks are active participants in the SWIFT gpi network which has improved cross-border wire tracking.

STC Pay: The Dominant E-Wallet

STC Pay (operated by STC, Saudi Arabia's dominant telecom) is the leading digital wallet in Saudi Arabia with approximately 12 million users in Saudi Arabia and 8 million across the Middle East, holding a 26% share of the Saudi digital wallet market. STC Pay functions as a stored-value wallet, IBAN-based bank transfer capability, and money transfer product — including international remittance to Pakistan, India, the Philippines, and other expatriate corridors that are economically significant given Saudi Arabia's large foreign worker population.

STC Pay received a SAMA digital banking license in principle in 2021 and was subsequently restructured under stc Bank, with full operational SAMA approval landing around 2024. This allows STC Pay/stc Bank to offer savings accounts, debit cards (STC Pay Visa co-badged), and consumer finance products — moving beyond pure wallet functionality toward a full digital banking proposition.

STC Pay for operators: STC Pay offers merchant acceptance via QR code and online API. Merchants with significant Saudi consumer exposure should treat STC Pay acceptance similarly to WeChat Pay in China or PayPay in Japan — the user base is large enough that non-acceptance represents a measurable conversion drag. Major payment aggregators operating in Saudi Arabia (HyperPay, Checkout.com, Tap Payments) include STC Pay in their payment method portfolio.

Apple Pay adoption: Saudi Arabia has exceptionally high Apple Pay adoption for a non-Western market. Apple Pay penetration among Saudi smartphone users is estimated at 40%+, driven by high iPhone market share and a consumer demographic with strong preference for contactless payments. Operators with in-app payment flows should prioritize Apple Pay support as a near-universal checkout option for Saudi iOS users.

Fintech Saudi and the SAMA Sandbox

SAMA's regulatory approach to fintech has been one of the more liberalized in the Gulf Cooperation Council (GCC). The Fintech Saudi initiative — a joint program between SAMA and the Capital Market Authority (CMA) — provides a formal sandbox for payment and financial services startups to test regulated activities under a controlled regulatory exemption.

The sandbox covers payment services, account aggregation, open banking, and digital lending. Foreign companies can participate in the Fintech Saudi sandbox with a Saudi presence requirement. Timeline from sandbox application to approval is typically 3–6 months.

SAMA licensing for payment operators: Operating a payment service (payment gateway, e-wallet, money transfer) in Saudi Arabia requires a SAMA license. The relevant licenses:

- Payment Service Provider (PSP) license: For entities operating a payment gateway, POS acquiring, or online payment platform

- Electronic Money Institution (EMI) license: For entities issuing stored-value products

- Money Transfer Operator (MTO) license: For cross-border remittance operators

Minimum capital requirements and compliance program requirements apply for each license category. Timeline for SAMA licensing is typically 6–18 months. Foreign-owned entities can hold SAMA payment licenses, subject to Saudi company registration and compliance with the Companies Law.

The ban on cash-only businesses: A SAMA regulation in force since 2018 prohibits merchants from refusing electronic payment methods. Businesses operating in Saudi Arabia must accept at least one non-cash payment method. This mandate, combined with the Mada acceptance requirement, means Saudi Arabia has among the highest mandatory payment acceptance coverage of any market in the MENA region.

Acquiring Partners: Entry Points for Foreign Operators

For foreign operators accessing Saudi Arabia without a direct SAMA license, the practical entry points are:

International acquirers with Saudi Arabia coverage:

- Checkout.com: Licensed payment institution in Saudi Arabia, providing card acquiring (Visa, Mastercard, Mada), STC Pay, Apple Pay, and BNPL acceptance via a single integration. Checkout.com's Saudi Arabia presence includes a local entity and SAMA license.

- Adyen: Has Saudi Arabia coverage for card acquiring; Mada e-commerce acceptance available via Adyen's platform.

- Stripe: As of mid-2025, Stripe's Saudi Arabia coverage for local card acquiring and Mada is limited — operators using Stripe for Saudi collections should verify current coverage and consider supplementing with a local acquirer.

Local acquirers and aggregators:

- HyperPay (Saudi-founded, GCC focus): One of the most widely used payment gateways in Saudi Arabia, with Mada, Visa, Mastercard, AMEX, STC Pay, and Apple Pay support. Used by a large portion of Saudi e-commerce merchants.

- Tap Payments (Kuwait-founded, GCC coverage): Covers Saudi Arabia with Mada, international cards, and wallet acceptance. Developer-friendly API.

- Paylink (Saudi-based): Focused on Saudi SME market, simpler integration model.

For operators choosing an acquiring partner: Confirm Mada e-commerce support explicitly — not all international acquirers have Mada Pay enabled in their Saudi product. Confirm settlement currency options (SAR settlement vs USD settlement) and settlement timelines. Saudi Arabia's standard settlement is T+1 for card transactions.

What This Means for Operators

Saudi Arabia is a large, fast-growing, and relatively high-income consumer market — Saudi GDP per capita exceeds $32,000 and e-commerce penetration is growing faster than most emerging markets. The payment infrastructure is modern: SARIE real-time rails, Mada acceptance at 95%+ of merchants, high Apple Pay penetration, and an active digital wallet market.

The entry requirements are specific:

- Mada acceptance is mandatory and requires an acquirer with Mada licensing — verify this before going live

- STC Pay acceptance is commercially important for consumer-facing operators

- Apple Pay support is high-ROI for mobile checkout

- SAMA licensing is required for operators wanting to hold customer funds or operate as a payment intermediary rather than just using a licensed acquirer

The Fintech Saudi sandbox provides a structured path for operators wanting to explore direct licensing without full upfront commitment. For operators who want market access faster, HyperPay or Checkout.com provide the cleanest turnkey entry with Mada, STC Pay, and Apple Pay coverage in a single integration.

Vision 2030's payment digitization ambitions have created a favorable regulatory environment for digital payment operators. The combination of regulatory support, high consumer digital payment adoption, and a growing e-commerce market makes Saudi Arabia one of the higher-return market entries in the MENA region for operators who invest in the correct payment stack from the outset.