Chargeback Management Compared: Alerts, Representment, and Recovery Models

Chargeback management compared by operating model: network pre-dispute alerts (Verifi, Ethoca), representment automation, managed recovery, and in-house.

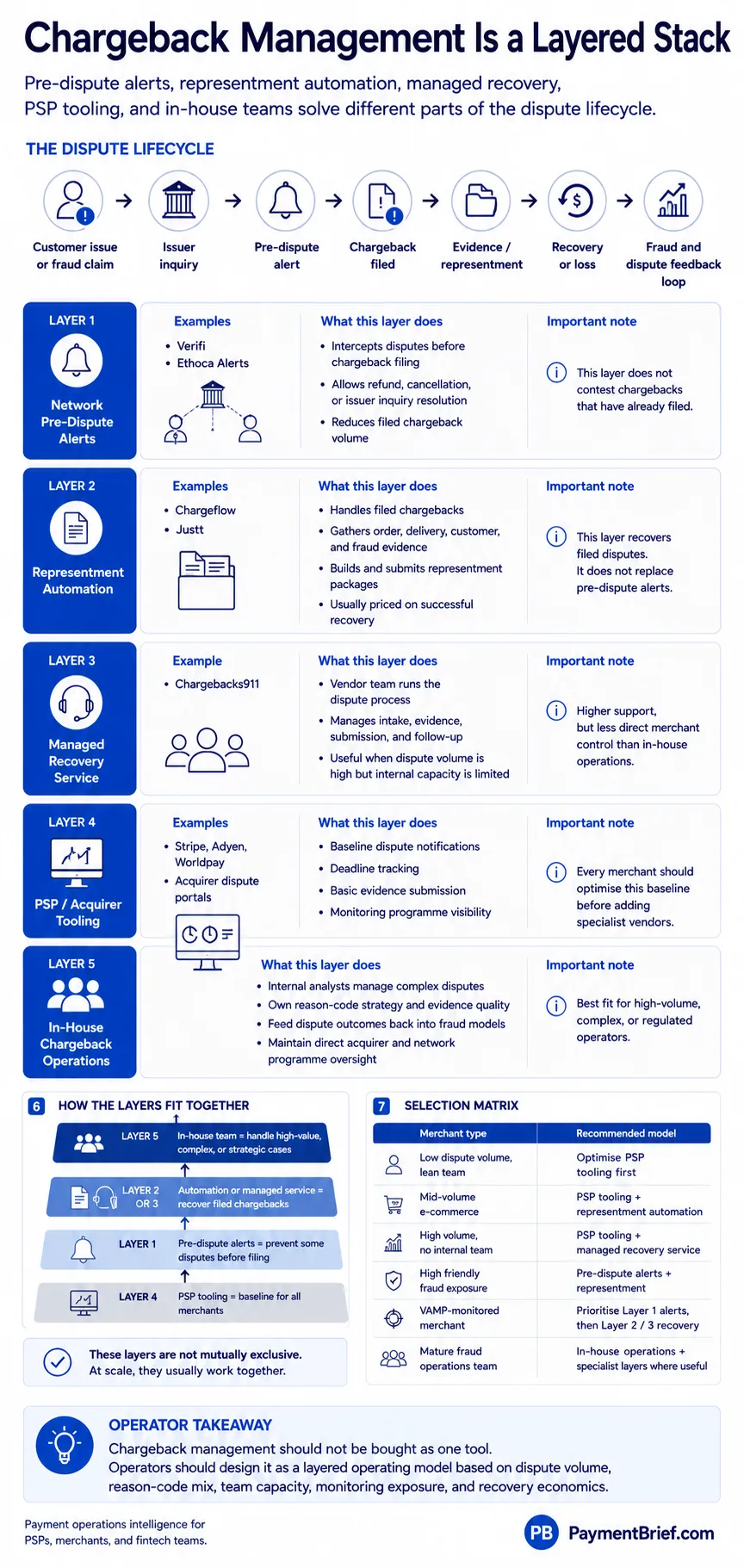

Chargeback management is a layered operating stack, not a single product category: network pre-dispute alerts, representment automation, managed recovery services, PSP tooling, and in-house operations. Match layers to your dispute volume, reason-code mix, and team capacity.

Chargeback management is not a single product category — it is a layered operating stack, and most operators use several layers at once. Network-side pre-dispute tools (Visa's Verifi, Mastercard's Ethoca Alerts) stop disputes before they become chargebacks, accessed through your PSP or acquirer. Merchant-side representment automation (Chargeflow, Justt) contests chargebacks that do file, with the vendor handling evidence and submission. Managed recovery services (Chargebacks911) take a team-led approach rather than self-serve software. PSP and acquirer dispute tooling is the baseline every operator already has. In-house operations remain the control-maximum alternative. The right combination depends on your dispute volume, reason-code mix, team capacity, and margin — not on a single vendor comparison.

Chargeback management is typically evaluated as a vendor selection problem. It is not. The operative question is which operating layers your dispute volume, reason-code mix, and team capacity justify — and how those layers fit together. Operators who evaluate Verifi and Chargeflow as if they are competing alternatives for the same job are solving the wrong problem.

Five operating models exist in the chargeback management space. They address different stages of the dispute lifecycle, have different cost structures, and are frequently used together rather than instead of each other.

The five operating layers

Before mapping vendors, the lifecycle matters. A dispute can be intercepted at three moments: before the cardholder contacts their issuer (rare), at the point of issuer inquiry before a chargeback is filed (Layer 1's window), and after the chargeback has been filed (Layers 2–3's territory). Understanding which stage a tool operates in determines what it can and cannot do for you.

Layer 1 — Network pre-dispute alert and deflection. Infrastructure that operates before a chargeback is filed, enabling the dispute to be resolved or deflected at the point of issuer or cardholder inquiry. These are network-side programs, not merchant SaaS.

Layer 2 — Merchant-side representment automation. Software the merchant configures to automatically gather evidence and submit representment for chargebacks that have been filed. The merchant retains strategic control; the software handles execution.

Layer 3 — Managed recovery / done-for-you chargeback operations. A service the vendor's team runs on the merchant's behalf. The merchant is a client; the vendor's analysts manage disputes as an outsourced function.

Layer 4 — PSP and acquirer-integrated dispute tooling. The dispute management interface and tooling built into the merchant's existing payment processor or acquirer. Every merchant already has this; it is the baseline.

Layer 5 — In-house chargeback operations. Dedicated internal analysts managing disputes using the merchant's own processes, tooling, and data. Maximum control at the cost of headcount and infrastructure.

Layer 1 — Network pre-dispute alert and deflection

Two distinct network programs operate at this layer: Verifi's portfolio of dispute-prevention products (Visa-owned) and Ethoca Alerts (Mastercard-owned). Both are pre-dispute collaboration infrastructure — they work before a chargeback is filed, not after.

Important framing: Verifi and Ethoca are not merchant SaaS products in the same category as Chargeflow or Chargebacks911. They are network programs that merchants access via their PSP, acquirer, or directly through a portal or API. The operational position is different: rather than a merchant contesting a chargeback, the merchant is receiving a pre-dispute signal from the issuer and resolving the dispute before it converts into a chargeback.

Verifi (Visa)

Verifi publicly positions three products, all operating before a chargeback files and all accessed by merchants directly or through their acquirer (accessed 2026-05-30):

Order Insight shares 120+ order data points with issuers in real-time inside Visa Resolve Online (VROL) at the point of customer inquiry. When an issuer receives a customer dispute inquiry and accesses VROL, Order Insight surfaces the merchant's transaction data — itemised receipt, delivery confirmation, customer service interaction history — enabling the issuer to resolve the inquiry without filing a chargeback. Disputes deflected here do not count against Visa's dispute ratio.

RDR (Rapid Dispute Resolution) automates the deflection decision using merchant-defined rules. Rather than requiring manual merchant response, RDR routes the pre-dispute through the Visa network and acquirer to automatically apply the merchant's configured resolution — a credit or a contest — in real time. Verifi describes it as "the only dispute management service providing automated real-time dispute resolution at the point of customer inquiry."

CDRN (Cardholder Dispute Resolution Network) is a manual, card-brand-agnostic channel: the merchant receives a dispute notification and has 72 hours to initiate a cardholder credit before the dispute files as a chargeback. CDRN operates across Visa and non-Visa networks (Mastercard, Discover, Amex). Disputes resolved via CDRN or RDR are not eligible for re-dispute.

Typical implementation is hours to 14 days. Access is direct through Verifi or via the merchant's acquirer.

Ethoca Alerts (Mastercard)

Ethoca Alerts, a Mastercard program, is a collaborative tool connecting merchants, acquirers, and issuers to share fraud and dispute data in near-real-time. Per Ethoca's public positioning (accessed 2026-05-30): the issuer initiates the alert when a cardholder reports fraud or a dispute; the alert reaches the merchant via a secure portal or API; the merchant resolves the case pre-chargeback — typically by issuing a refund or cancelling the order. Consumer Clarity is an associated Mastercard product; it received minimal detail on reviewed public pages.

The layer-1 access model: neither Verifi nor Ethoca is a standalone SaaS subscription in the way Chargeflow or Chargebacks911 is. Access paths run through the card network, the acquirer, or direct API integration. If you are evaluating these programs, your acquirer or PSP's support for the relevant integration is a prerequisite to discuss before evaluating coverage.

What Layer 1 does not do: it does not contest chargebacks that have already been filed. It does not cover all dispute reason codes (issuer participation and reason-code eligibility vary). It does not replace representment for chargebacks that pass through to filing. For the full mechanics of how Visa and Mastercard dispute programs interact with merchant operations, and the reason code reference for Visa and Mastercard, those articles cover the regulatory structure in detail — or look up a single code directly in the reason-code lookup tool.

Layer 2 — Merchant-side representment automation

Representment automation software handles chargebacks that have been filed: the platform ingests the dispute, gathers evidence (order data, delivery records, prior customer contact, fraud signals), builds the representment package, and submits it within the card network's deadline — automatically, without requiring the merchant's team to work each case. For the mechanics of how AI-powered representment actually works — evidence models, CE 3.0 qualification, the LLM-vs-ML architecture — that article covers the implementation layer. This section focuses on which vendors sit here and how they differ from each other and from Layer 3.

Chargeflow publicly positions as fully automated, merchant-configured representment software (accessed 2026-05-30). The merchant controls which chargebacks Chargeflow manages; Chargeflow handles evidence gathering, packaging, and submission. Coverage spans Visa, Mastercard, Amex, and Discover reason codes per the product page. Pricing model (publicly disclosed): 25% per recovered chargeback, contingency-only, no long-term contracts. Verify the current rate at evaluation time.

Justt publicly positions as AI-powered representment automation with a contingency pricing model — the platform charges only on successful recovery (accessed 2026-05-30). The merchant defines strategy and can override individual decisions; Justt handles execution. Networks supported: Visa and Mastercard (VAMP and SMMP programs mentioned). Integrations include Adyen, Stripe, Braintree, Chase, and Shopify. Pricing rate not publicly disclosed.

Both are software the merchant configures, not teams that run your chargeback operations. The distinction from Layer 3 is structural, not just operational — see below.

Layer 3 — Managed recovery and done-for-you chargeback services

Managed recovery vendors operate the same representment and recovery function as Layer 2, but as a team-led service rather than software the merchant runs. The merchant is a client; the vendor's analysts handle dispute intake, evidence, submission, and follow-up.

Chargebacks911 publicly positions as "Full-Service Dispute Management" — a team-led managed service, not self-serve automation (accessed 2026-05-30). Client testimonials on the homepage emphasise the Chargebacks911 team taking action. Networks covered: Visa, Mastercard, PayPal. A "performance guarantee" is stated on the homepage; terms are not publicly disclosed — require them in writing. Pricing is contact-required.

The software-vs-service distinction matters practically: representment automation (Layer 2) scales with volume at a per-recovery rate, gives the merchant direct oversight of the evidence and strategy, and requires some internal knowledge to configure. Managed services (Layer 3) may include advisory, escalation handling, and strategic guidance that software alone does not provide, at the cost of less direct control and potentially a more complex vendor relationship. Neither is universally superior — fit depends on your internal fraud-ops maturity, dispute complexity, and bandwidth.

Layer 4 — PSP and acquirer-integrated dispute tooling

Every operator already has this layer. PSP and acquirer dispute portals — built into your existing payment infrastructure — provide:

- Dispute notifications and deadline tracking

- Basic evidence submission against card network deadlines

- Dispute ratio and monitoring programme threshold visibility

- Automated response templates for common dispute types

This is the correct baseline for any chargeback management evaluation. Before adding any specialist Layer 1–3 tool, operators should understand what their PSP tooling already covers, what reason codes it handles automatically, and what its representment win rates look like segmented by reason code — not blended. The true cost of a chargeback article covers the unit economics that determine when the cost of adding a specialist layer is justified.

Layer 5 — In-house chargeback operations

In-house chargeback teams manage disputes using the merchant's own analysts, processes, tooling integrations, and internal data. This model delivers maximum control — over evidence strategy, reason-code specialisation, the feedback loop from dispute outcomes into fraud model training, and the merchant's relationship with acquirers and network programme managers.

The practical case for in-house is strongest when:

- Dispute volume is high enough to justify dedicated analyst headcount at lower per-case cost than vendor contingency fees

- Fraud and chargeback patterns are complex enough that generic representment logic consistently underperforms

- Closing the feedback loop from dispute outcomes to fraud model training is a priority (easiest when both are in-house)

- Regulatory or compliance requirements mandate internal control over how disputes are handled

Most merchants operate in-house alongside specialist layers rather than instead of them — using PSP tooling as the baseline, Layer 1 programs for pre-dispute deflection, and specialist representment or managed services for the dispute population that passes through.

How the layers fit together

These layers are not mutually exclusive. A layered chargeback operation is the norm at scale, not the exception.

A worked example of a layered setup:

- Layer 4 (PSP tooling) handles the baseline — auto-responding to obvious representable disputes within the deadline.

- Layer 1 (Verifi Order Insight + Ethoca Alerts) intercepts a subset of disputes before they file, reducing total chargeback volume.

- Layer 2 or 3 (Chargeflow, Justt, or Chargebacks911) contests the chargebacks that pass through Layer 1 and are not auto-handled by the PSP.

- In-house analysts (Layer 5) handle high-complexity disputes, chargebacks above a threshold value, and cases requiring merchant-specific evidence not available to an external vendor.

The decision of which layers to activate is fundamentally an economics problem: what is the cost of each layer (contingency fee, setup, integration, headcount), what is the dispute volume and reason-code mix it addresses, and what is the marginal revenue recovered versus the current baseline? For the underlying economics, see the chargeback operations KPI scorecard and the true cost of a chargeback.

Vendor comparison

Sourcing note: all claims in this table are drawn from vendor product pages accessed 2026-05-30. Re-verify at evaluation time. Performance metrics (win rates, recovery rates, alert reduction %, ROI figures) are excluded — these are vendor-reported, vary by merchant traffic base, and are not independent benchmarks.

| Dimension | Verifi (Visa) | Ethoca Alerts (Mastercard) | Chargeflow | Justt | Chargebacks911 |

|---|---|---|---|---|---|

| Operating layer | Layer 1 — network pre-dispute | Layer 1 — network pre-dispute | Layer 2 — representment automation | Layer 2 — representment automation | Layer 3 — managed recovery service |

| Lifecycle stage | Before chargeback files | Before chargeback files | After chargeback files | After chargeback files | After chargeback files |

| Network affiliation | Visa-owned | Mastercard-owned | Independent | Independent | Independent |

| Access model (publicly stated) | Direct or via acquirer/PSP; portal or API; hours–14 days implementation | Via Mastercard network; secure portal or API | Direct merchant integration; 45+ PSP integrations stated | Direct; Adyen, Stripe, Braintree, Chase, Shopify integrations stated | Managed onboarding; verify directly |

| Who manages the process | Merchant responds to alerts or sets RDR rules; network/acquirer executes | Merchant responds to issuer-initiated alerts | Chargeflow manages execution; merchant controls scope | Justt handles execution; merchant sets strategy | Chargebacks911 team manages cases |

| Pricing model (publicly stated) | Not publicly disclosed; verify via acquirer/Verifi | Not publicly disclosed; verify via Mastercard/acquirer | 25% per recovered chargeback; contingency only; no long-term contract | Contingency (rate not disclosed; fee on recovery only) | Contact-required; not publicly disclosed |

| Chargeback liability assumption | No | No | No | No | "Performance guarantee" stated; terms not public |

| Substitute for other layers? | No — complements Layers 2–3; covers different lifecycle stage | No — complements Layers 2–3; covers different lifecycle stage | No — Layer 1 still valuable for dispute prevention | No — Layer 1 still valuable for dispute prevention | No — Layer 1 still valuable for dispute prevention |

Selection matrix by merchant archetype

| Archetype | Recommended layers | Rationale |

|---|---|---|

| Low dispute volume, lean team | Layer 4 (PSP tooling) only — optimise before adding specialist layers | The marginal revenue from specialist layers may not justify the cost or integration overhead at low volume. Optimise PSP tooling first. |

| Mid-volume e-commerce, no in-house fraud team | Layer 4 + Layer 2 (representment automation) | Chargeflow or Justt help contest filed chargebacks and seek recovery without requiring analyst headcount. Add Layer 1 once the representment layer is stable and you can measure pre-dispute deflection incremental value separately. |

| High dispute volume, no internal chargeback team | Layer 4 + Layer 3 (managed recovery service) | Chargebacks911's team-led model handles complexity and volume without requiring internal analyst capacity. Evaluate adding Layer 1 programs in parallel once the managed service is established. |

| High first-party fraud / friendly fraud exposure | Layer 1 + Layer 2 or 3 | First-party fraud generates disputes that Layer 1 programs can sometimes deflect at the issuer inquiry stage — before the chargeback files. Combine with representment for disputes that file despite deflection attempts. |

| VAMP-monitored merchant (elevated fraud-to-sales ratio) | Layer 1 programs are highest priority; then Layer 2–3 for filed disputes | Pre-filing dispute deflection can reduce filed chargeback volume, but operators should verify how each program affects Visa VAMP, Mastercard monitoring, and acquirer-level reporting — Verifi is Visa-owned infrastructure, while Ethoca is Mastercard-owned, and their effects on scheme monitoring ratios differ. See the VAMP monitoring article for Visa ratio mechanics. For remediation steps once monitoring has triggered, see VAMP Remediation Checklist. |

| Mature fraud team with in-house operations | Layer 5 as primary; Layer 1 programs for pre-dispute deflection; evaluate Layer 2 for high-volume low-complexity dispute categories | Internal teams handle complex, high-value disputes and own the feedback loop to fraud detection. Layer 1 reduces volume. Layer 2 automation may reduce per-case handling effort for routine, high-volume dispute categories, while in-house analysts remain better suited to complex or high-value cases. |

What public pages do not tell you — ask in the RFP

The comparison table covers publicly verifiable positioning. The following determine day-to-day operational reality and financial exposure — none are disclosed on product pages.

Layer 1 (Verifi, Ethoca Alerts)

- What proportion of your issuers actively participate in the pre-dispute program — by card network, region, and dispute type?

- Which chargeback reason codes qualify for deflection versus which must proceed to representment?

- What data submission requirements must be met for deflection to function (missing fields reduce effectiveness significantly)?

- What is the implementation path for your specific acquirer or PSP — and does your acquirer already support these integrations?

- For RDR: what are the rule configuration constraints, and what happens to disputes your rules do not match?

Layers 2–3 (Chargeflow, Justt, Chargebacks911)

- What is your win rate segmented by reason code, card network, and dispute category — not blended across all disputes?

- Which dispute categories are excluded from the contingency fee or performance guarantee?

- What are your submission deadline SLAs by card network — and what happens if you miss a deadline?

- How do dispute outcome data flow back into your model for future improvement — and how long is the feedback lag?

- For managed services: who at your firm reviews and approves the representment strategy for individual cases, and what is the escalation path for high-value disputes?

- What are the full contract terms: cancellation notice, minimum volume commitments, guarantee scope and exclusions?

For all vendors

- What happens to disputes in categories your tool does not cover — who handles them, and at what cost?

- How does your tool integrate with our fraud detection and order management systems, and what data does it require?

- What are your regional coverage limitations — geography, currency, payment method?

- What is your data processing and privacy framework for non-US merchants?

What this article does not cover

Performance numbers — win rates, alert reduction percentages, ROI figures — are absent by design. All figures in this space are vendor-reported, vary by merchant, dispute mix, and integration quality, and are not independently audited. For measuring your own chargeback operations once a platform is in place, see the chargeback operations KPI scorecard.

For the mechanics of how AI representment and automated evidence gathering work, see AI chargeback representment automation.

For the upstream fraud platform decision — which determines how many chargebacks reach chargeback management in the first place — see the sibling buyer's guide: fraud prevention platforms compared.

For the scheme rule context that Layer 1 programs operate within, see Visa VCR and Mastercard Mastercom rules in 2026.

Sources & methodology (8)

Verifi Order Insight shares 120+ order data points with issuers in real-time inside Visa Resolve Online (VROL) to deflect disputes at the point of customer inquiry before a chargeback is filed

Checked:

Verifi RDR (Rapid Dispute Resolution) provides automated real-time dispute resolution at the point of customer inquiry, routing through Visa network and acquirer; only service of its kind at network level

Checked:

Verifi CDRN is a manual, card-brand-agnostic pre-dispute solution; merchant has 72 hours to initiate a cardholder credit before a chargeback files; disputes resolved via CDRN or RDR do not count against Visa's dispute ratio

Disputes resolved via CDRN or RDR are not eligible for future re-dispute per Verifi documentation

Checked:

Ethoca Alerts is described as a collaborative tool connecting merchants, acquirers, and issuers to share fraud and dispute data; issuer-initiated; merchants access via secure portal or API through the Mastercard network

Checked:

Chargeflow publicly positions as fully automated merchant-side representment; merchant controls which chargebacks Chargeflow manages; covers Visa, Mastercard, Amex, Discover reason codes

Checked:

Chargeflow pricing model: 25% per recovered chargeback, contingency-only, no long-term contracts — publicly stated on product page

Vendor-disclosed pricing; verify at time of evaluation as rates are subject to change

Checked:

Justt publicly positions as AI-powered representment automation with contingency pricing; merchant defines strategy and can override; Visa and Mastercard networks; integrates with Adyen, Stripe, Braintree, Chase, Shopify

Contingency pricing rate not publicly disclosed; fee charged only on successful recovery

Checked:

Chargebacks911 publicly positions as full-service managed dispute management run by their team, not self-serve automation; covers Visa, Mastercard, PayPal; states a performance guarantee on homepage — terms not publicly detailed

Pricing contact-required; guarantee terms not publicly disclosed — verify scope, exclusions, and SLAs directly

Checked:

Source types explained in our Methodology.