MoR Provider Guide: Paddle, Polar, FastSpring, and Lemon Squeezy

Paddle, Lemon Squeezy, Polar & FastSpring compared by tax footprint, coverage, and fit — how to choose the Merchant of Record matched to your seller type.

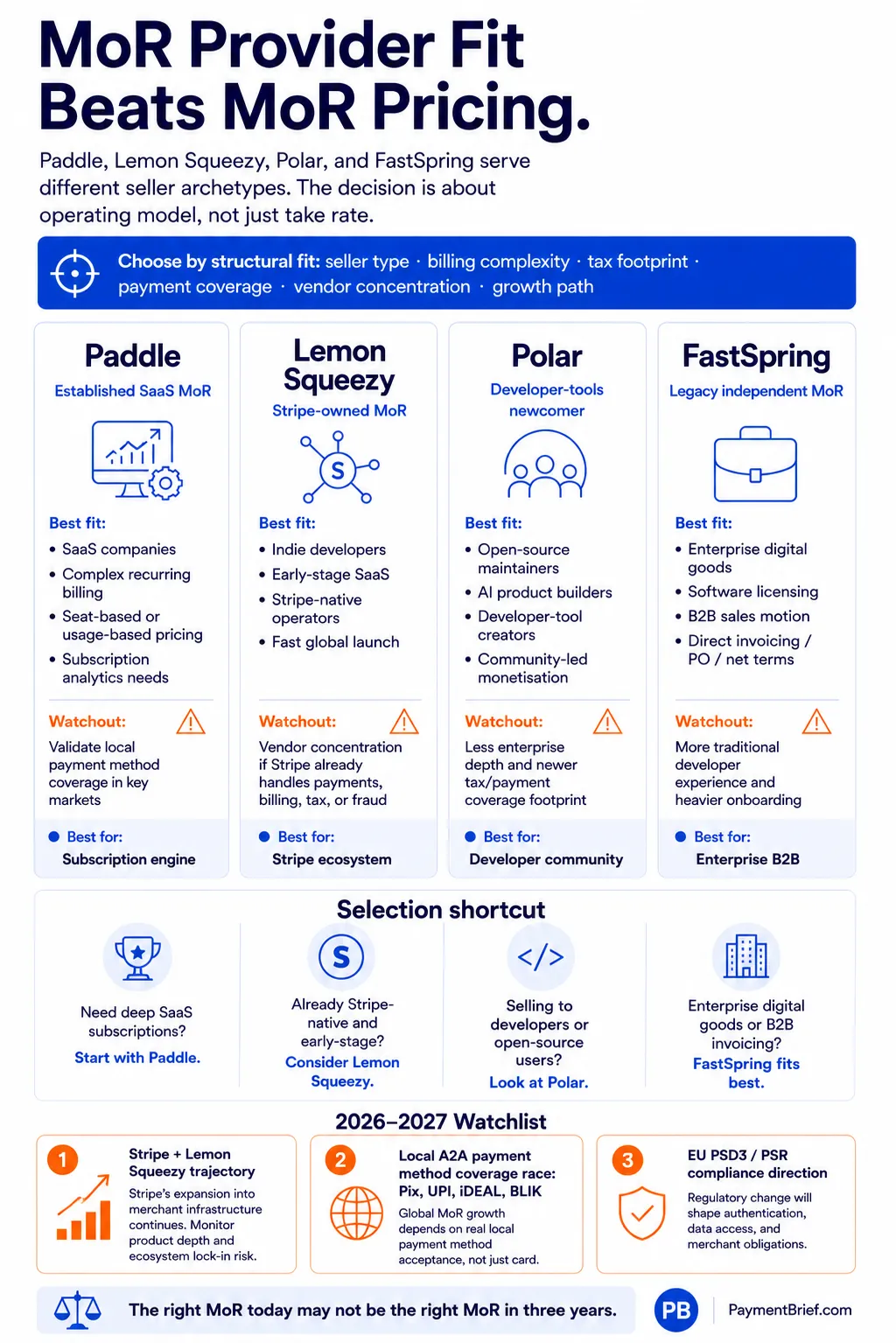

Paddle, Lemon Squeezy (now Stripe-owned), Polar, and FastSpring compared by coverage, tax footprint, DX, and strategic fit — not pricing. The right MoR isn't the cheapest; it's the one whose structural trade-offs match your seller archetype and growth trajectory.

The four primary Merchant of Record providers serving software and digital product companies differ not on price but on structural fit. Paddle is the established pure-play MoR built for SaaS recurring billing, with deep subscription management tooling and an enterprise push through its ProfitWell acquisition. Lemon Squeezy, acquired by Stripe in July 2024, is the MoR option inside the Stripe ecosystem — Stripe can now offer both MoR and direct PSP processing under one corporate roof, potentially operating the transition between them as a product. Polar is a Y Combinator-backed newcomer positioned specifically for open-source developer tools, AI products, and developer-community monetisation. FastSpring is the independent MoR with the longest operating history, serving enterprise digital goods companies that want an MoR not affiliated with a card-processing PSP.

The MoR provider market has consolidated around four primary options for software and digital product companies, each occupying a distinct position within the broader PSP and infrastructure landscape. For the past several years, selecting one meant comparing published pricing tables — a comparison that became less useful every time a provider revised its fee structure. The more durable framework is structural fit: what each provider is built for, who controls it, and which trade-offs it makes in exchange for what it offers.

This piece does not compare pricing. Published take rates change more often than a published article can track, and the delta between providers is rarely the deciding factor — the deciding factor is usually whether the provider supports the payment methods your customers expect, whether its recurring billing tooling handles your subscription structure, and whether its ownership and trajectory create or resolve vendor concentration risk.

Paddle: The Established Pure-Play

Paddle is the closest thing the MoR space has to an established category leader for SaaS. Founded in the UK in 2012 and headquartered in London and New York, Paddle's core product was built around software subscription billing from the beginning — it is MoR-first, not a PSP that added MoR as a feature.

The structural depth this creates is in subscription management. Paddle handles proration, upgrade and downgrade flows, trial management, pause and resume, dunning, and failed-payment recovery natively. For a SaaS company with seat-based pricing, annual plans with monthly instalments, or multi-currency subscription catalogs, Paddle's billing engine is meaningfully deeper than what a generic PSP integration with a separate billing layer produces.

The ProfitWell acquisition in May 2022 was the signal of Paddle's enterprise direction. ProfitWell's subscription analytics and revenue reporting tooling — retention metrics, MRR/ARR decomposition, churn analysis — integrated into Paddle's platform gives Paddle accounts a data layer that most MoRs don't offer. This is consistent with a push upmarket: Paddle is increasingly pursuing larger SaaS companies where the MoR value proposition is not just "we handle your taxes" but "we are your subscription revenue infrastructure."

What Paddle is not well-suited for: very high-volume low-value digital transactions (where the MoR premium bites hardest per transaction), pure marketplace models (sellers selling to buyers with complex payout flows), and operators who specifically want an MoR not affiliated with the broader Stripe ecosystem. On that last point: Paddle is independent, not owned by a PSP group — which is a structural differentiator from Lemon Squeezy post-acquisition.

Local payment method coverage is an area to verify per market at evaluation time. Paddle supports a broad range of card networks and major wallets, with incremental additions of local A2A rails. Markets with dominant non-card payment methods — Brazil (Pix), India (UPI), Netherlands (iDEAL), Poland (BLIK) — should be validated directly with Paddle's current support matrix before committing.

Lemon Squeezy: The Stripe-Owned MoR

Lemon Squeezy entered the MoR market as the most developer-friendly option at the entry tier — simple API, straightforward onboarding, and a product experience that resonated with indie developers and early-stage SaaS founders. Stripe's acquisition in July 2024 changed the strategic calculus for every operator evaluating it.

The acquisition created something that did not previously exist: a single corporate entity offering both a Merchant of Record product (Lemon Squeezy) and a direct PSP processing product (Stripe Payments). This is strategically significant because it lets Stripe offer the migration between the two as a product, not a vendor change.

The bull case for Lemon Squeezy post-acquisition: Stripe can invest in it at a scale an independent MoR cannot match, and operators who are already deep in the Stripe ecosystem (Stripe Billing, Stripe Tax, Stripe Radar) get a smoother on-ramp. If you are already Stripe-native and want to add MoR for a global launch, Lemon Squeezy inside Stripe is a coherent path.

The bear case: vendor concentration. If you already process through Stripe Payments, adding Lemon Squeezy means your entire payment infrastructure — processing, billing, MoR — sits within one corporate group. For operators who view vendor diversification as a risk management principle, this is a structural concern. Paddle and FastSpring remain independent; choosing either means your MoR counterparty is not affiliated with your primary PSP.

The secondary concern is product trajectory. Stripe could integrate Lemon Squeezy deeply into its platform in ways that are beneficial (more features, better data connectivity) or consolidating (reduced independent identity, eventual absorption into Stripe Tax or Stripe Billing in ways that increase switching costs). Operators choosing Lemon Squeezy should maintain clean data exports as a standard practice and validate periodically that customer and transaction data remains portable.

For the specific audience Lemon Squeezy was designed for — indie developers and small bootstrapped SaaS — the product continues to work well. The strategic question applies more to companies scaling into the stage where vendor concentration becomes a board-level discussion.

Polar: The Developer-Tools Newcomer

Polar is the newest entrant in this list and the most narrowly positioned. Y Combinator-backed and built specifically for open-source maintainers, developer-tool creators, and AI product builders, Polar's MoR service wraps around a creator-economy framing that the other three providers do not address.

The use cases Polar targets: an open-source library maintainer who wants to add a paid tier; an AI tool builder selling API credits to developer users; a developer selling a technical course, template library, or plugin pack; a software creator running a community subscription. These are transaction patterns where the buyer is typically a developer or technical buyer, the product is often digital-native, and the sales motion is community-led or developer-community-led rather than sales-team-led.

Polar's integration surface is deliberately lightweight — the API and SDK are built for technical founders who want to go from zero to accepting payments without a large integration project. This trade-off is intentional: Polar has less subscription management depth than Paddle, less enterprise B2B tooling than FastSpring, and less ecosystem breadth than Stripe/Lemon Squeezy. What it offers instead is a product experience tuned specifically for the open-source and developer-community monetisation pattern.

For operators outside that specific archetype — a SaaS company with a sales team, seat-based enterprise contracts, or complex multi-currency subscription flows — Polar is not the right fit. For the archetype it targets, it is arguably the most specifically designed option in the market.

Tax footprint and payment method coverage are areas where Polar, as a newer entrant, may trail the more established providers in specific markets. Verify current coverage at evaluation time.

FastSpring: The Legacy Independent

FastSpring is the MoR that has operated longest in this space, serving digital software and goods companies with an enterprise-grade product and a positioning that emphasises independence.

The independence point matters to a specific buyer: operators who want an MoR counterparty that is not owned by a card-processing PSP, not affiliated with an ecosystem that creates cross-product switching costs, and not a startup still finding product-market fit. FastSpring is none of those things — it is an established independent business with a track record in enterprise digital goods.

FastSpring's heritage is in software licensing, game sales, and enterprise digital products — a different starting point from Paddle's SaaS-subscription origin. This shapes where its product is strongest: handling high-value single-purchase software licences, enterprise B2B digital goods transactions where invoicing requirements are specific, and digital goods sellers with a mix of subscription and one-time purchase models.

Where FastSpring trails the newer providers: developer experience and API modernity. The integration experience is more traditional than Polar's or Lemon Squeezy's; onboarding is more involved; the product is built for companies with an implementation resource, not solo founders who want same-day go-live. This is not necessarily a weakness — it reflects a product built for the buyer who wants depth over simplicity.

FastSpring on the enterprise B2B consideration: of the four providers, FastSpring has the most established track record handling enterprise digital goods transactions with direct invoicing, purchase-order-based workflows, and net-term billing arrangements that enterprise buyers often require. For operators whose primary market is enterprise B2B, FastSpring's positioning is the closest structural match.

The Selection Matrix

For a fast operator scan:

| Provider | Best fit | Main caveat |

|---|---|---|

| Paddle | SaaS with complex recurring billing — seat- or usage-based, subscription depth | Verify local payment-method coverage (Pix/UPI/iDEAL/BLIK) per market before committing |

| Lemon Squeezy | Indie devs / early-stage SaaS already in the Stripe ecosystem | Vendor concentration — processing, billing, and MoR all within one corporate group |

| Polar | Open-source, AI, and developer-tool creators selling via community-led motion | Less enterprise/subscription depth; newer, so verify tax and payment-method coverage |

| FastSpring | Enterprise digital goods / B2B software; operators wanting PSP-group independence | More traditional onboarding and heavier implementation; not for same-day solo go-live |

The clearest way to choose across these four is to identify your primary seller archetype:

Indie developer or early-stage SaaS, global launch, Stripe ecosystem already in use: Lemon Squeezy is the path of least resistance. Understand the vendor concentration implication; mitigate with clean data portability habits.

SaaS company with complex recurring billing, seat-based or usage-based pricing, or enterprise ambitions: Paddle. The subscription management depth and ProfitWell analytics integration are purpose-built for this archetype.

Open-source maintainer, AI product builder, or developer-tool creator selling to a technical audience via community-led motion: Polar. The trade-off is less enterprise B2B depth; if that is not your market, the trade-off is worth it.

Enterprise digital goods seller, software company with B2B sales motion, or operator who specifically wants an MoR independent of any PSP group: FastSpring. The developer experience is more traditional, but the enterprise track record and structural independence are the differentiators.

Operator in multiple markets with dominant local A2A payment methods: validate current payment method support from all four providers before selecting. This is the variable most likely to override the other selection criteria — a provider that doesn't support the dominant payment method in your largest market is a structural blocker regardless of fit on every other dimension.

What to Watch in 2026–2027

The most consequential variable over the next 18–24 months is how Stripe chooses to position Lemon Squeezy relative to Stripe Tax and Stripe Payments. If Stripe moves toward a "choose your MoR or build-your-own compliance stack" product architecture — with Lemon Squeezy as the MoR path and Stripe Tax as the build-your-own path — it creates a compelling on-ramp-to-graduation product that no independent MoR can match. That trajectory benefits Paddle and FastSpring competitively only if operators value independence enough to pay for it.

The second variable is local payment method coverage race. As Pix, UPI, iDEAL, BLIK, and similar A2A rails grow as share of digital commerce in their respective markets, MoRs that have not supported those methods will face an increasingly hard cap on their addressable market in those geographies. Coverage parity — all four providers supporting the same local method set — is probably three to five years away; until then, local coverage is a real differentiator.

The third variable is EU regulatory direction. PSD3 and the Payment Services Regulation (PSR) being finalised in 2025-2026 may clarify or expand the compliance obligations that MoRs carry on behalf of their sellers in EU markets, potentially changing the relative value of the MoR model in Europe versus a direct-PSP-plus-tax-automation stack. Operators planning ahead should review the MoR migration playbook for Paddle, Polar, and Lemon Squeezy before the regulatory picture crystalizes.

The right provider today is not necessarily the right provider in three years — and when a Merchant of Record stops making sense is a question worth modeling before committing to any provider. The structural decision to use MoR at all — and when to migrate off — matters more than the provider selection within the MoR tier.

Sources & methodology (7)

Paddle acquired ProfitWell in May 2022 to integrate subscription analytics and revenue reporting into its MoR platform

Checked:

Stripe acquired Lemon Squeezy in July 2024; Lemon Squeezy continues to operate as a MoR product under Stripe

Checked:

Paddle positions itself as a Merchant of Record for SaaS and software companies, handling global VAT/GST, chargebacks, and payment processing

Checked:

Polar (Polar.sh) is a Y Combinator-backed MoR focused on developer tools, open-source monetisation, and AI product creators

Checked:

FastSpring is an independent MoR (not owned by a card-processing PSP group) serving digital goods and software companies

Checked:

EU One-Stop Shop (OSS) consolidates VAT filings for cross-border digital sales into one return per quarter, but underlying per-country VAT obligation remains

Checked:

Visa Acquirer Monitoring Programme chargeback thresholds apply at the MoR's MID level, not individual seller level — MoR absorbs aggregate chargeback risk

Checked:

Source types explained in our Methodology.