The MDR Stack: Reading Your Processing Statement Line by Line

The merchant discount rate is not a single fee — it's a five-layer stack. Here's what each layer is, who pays whom, what's negotiable, and how to decompose your own statement to find the margin you're leaving on the table.

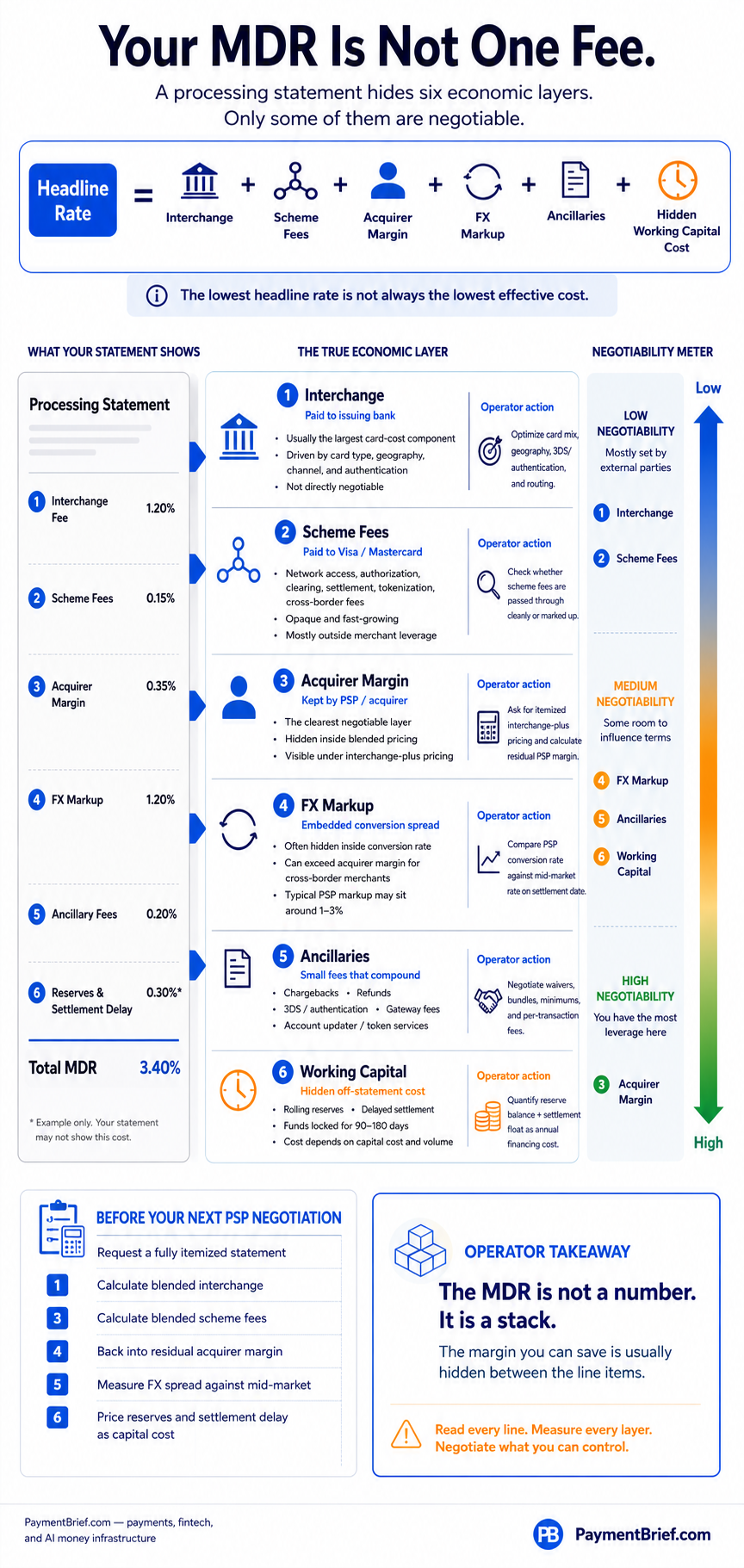

MDR decomposes into 5 fee layers — interchange, scheme fees, acquirer margin, FX markup, ancillaries — plus a sixth off-statement cost: working capital tied up by reserves and settlement timing. Acquirer margin, FX, ancillaries, and reserves are all negotiable to varying degrees.

The merchant discount rate is the headline number on every payments contract. It’s also the number that hides the most. When a PSP quotes you a flat 2.9% + 30¢, you are not buying one service at one price — you are buying a stack of services where the components have different owners, different economics, and very different negotiability. Some of those components are fixed by Visa or Mastercard and pass through at cost. Others are pure margin. Some never appear on the statement at all.

This briefing walks through every layer of the MDR stack, top to bottom. The goal is operational: by the end, you should be able to read your own processing statement and identify which line items you can move and which you cannot. The same framework applies whether you are evaluating a new PSP, negotiating a renewal, or trying to figure out where the margin actually went on a quarter you thought looked clean.

Layer 1 — Interchange

Interchange is the fee the acquirer (your PSP, in most cases) pays to the cardholder’s issuing bank on every card transaction. It is the largest single component of the MDR for most card types, typically 0.20–2.50% depending on geography, card type, transaction channel, and authentication method.

Interchange is set by Visa and Mastercard — not your PSP — and published in their interchange tables, which run to hundreds of pages and update twice a year (typically April and October). The structure matters operationally:

- Card type drives most of the variance. Premium consumer cards (Visa Infinite, Mastercard World Elite) carry interchange 2–3× higher than standard debit. Corporate and commercial cards are higher still. In the EU and UK, regulated consumer interchange is capped at 0.20% debit / 0.30% credit, but corporate cards sit outside the cap and routinely run 1.5–2.0%.

- Geography matters. US interchange is largely unregulated outside of debit (capped under Durbin at $0.21 + 0.05%). Australia caps credit interchange at 0.50%. Brazil caps at 0.50% credit / 0.80% debit. India runs MDR caps directly, not interchange caps.

- Authentication and channel matter. Card-not-present transactions carry higher interchange than card-present. 3DS2-authenticated transactions get a small interchange discount in most markets — typically 5–15 basis points — because the liability shifts to the issuer.

What this means for operators: interchange is the line item you cannot directly negotiate, but the mix of interchange you pay is shaped by decisions you control. Card type mix, geographic mix, channel (card-present vs not), and authentication strategy all move your blended interchange materially. A merchant whose customer base shifts toward premium credit cards will see interchange drift upward over time without changing anything else.

Layer 2 — Scheme Fees

Scheme fees are charged by Visa and Mastercard themselves for using the network — authorisation, clearing, settlement, brand licensing, fraud data, tokenisation services, and roughly 30 other line items that vary by network and have grown 20–30% since 2019. They are not regulated the way interchange is, which is why they have been the fastest-growing component of the MDR for the past five years.

The major categories on most statements:

- Network access / assessment fees. A percentage of volume (typically 0.10–0.15%) plus a small per-transaction fee. This is the base “tax” for being on the network.

- Authorisation fees. Charged per authorisation request, including declines. Pre-authorisation, partial authorisation, and reauthorisation each carry their own line items at most PSPs.

- Cross-border fees. When the issuer country differs from the acquirer country, Visa and Mastercard layer in a cross-border surcharge — typically 0.40–1.20% on top of standard scheme fees. This is what makes accepting a US-issued card in Singapore meaningfully more expensive than accepting a Singapore-issued card. Cross-border is not a separate stack layer — it is a category of scheme fee, plus an interchange uplift on the issuer side.

- Digital enablement fees. Tokenisation, 3DS2 processing, network token provisioning, and various “value-added” services. These are the line items that have grown fastest. Most are presented as bundled features but priced à la carte.

Card scheme fees demystified walks through the 30+ specific line items and what each one is for. The structural point is that scheme fees are opaque, growing, and largely outside merchant leverage except at very high scale — Visa and Mastercard negotiate rebates with merchants processing above roughly $1B annually in network volume, and not below.

Layer 3 — Acquirer Margin

This is the only layer that is yours to negotiate. The acquirer margin is what your PSP keeps after paying interchange to the issuer and scheme fees to the network. On a 2.9% blended rate, the acquirer margin is typically somewhere between 0.30% and 1.00% — but you cannot see it without asking for interchange-plus pricing.

The two pricing models matter here:

- Blended pricing (e.g., Stripe’s standard 2.9% + 30¢ in the US) bundles interchange, scheme fees, and acquirer margin into a single rate. You pay the same regardless of card type, which means the PSP keeps the spread on lower-cost cards (debit, regulated EU consumer) and absorbs the cost on higher-cost cards (premium credit, corporate). On most volume mixes, blended pricing leaves 0.50–1.50% with the PSP.

- Interchange-plus pricing (the standard at Adyen, Checkout.com, and Stripe above sufficient scale) passes interchange and scheme fees through at cost and adds a transparent acquirer margin on top. Typical interchange-plus margins: 0.10–0.50% plus $0.05–$0.30 per transaction, with the percentage compressing faster than the per-transaction fee as volume grows.

What good margin looks like depends on your scale. Below $1M monthly volume, expect 0.30–0.50% on interchange-plus. Above $10M monthly, sub-0.20% is achievable for low-risk verticals. Above $50M monthly, margins below 0.10% are common with multi-acquirer routing for leverage. The PSP negotiation playbook covers what leverage actually moves the margin at each scale.

The practical takeaway: if your PSP refuses to show interchange and scheme fees as separate line items, you cannot tell what you are paying for. That refusal is itself a negotiating signal.

Layer 4 — FX Markup

When a cardholder pays in a currency that differs from your settlement currency, the PSP performs a conversion at a rate that includes a markup over mid-market. Typical PSP FX markup runs 1–3%, embedded in the quoted conversion rate rather than disclosed as a separate fee.

This is often the single largest variable cost for operators with cross-border volume, and the easiest to underestimate. A merchant processing $1M/month in cross-currency transactions at a 2% embedded FX markup pays $240K/year in invisible conversion costs — frequently larger than the entire acquirer margin.

To measure your own FX markup, compare the conversion rate the PSP applied to the same transaction’s mid-market rate at the time of settlement. The ECB reference rate works for EUR; Bloomberg’s mid-market for other major currencies. The difference, divided by the transaction amount, is your effective FX spread.

Negotiating leverage on FX:

- Below $500K monthly in cross-currency volume, most PSPs hold the embedded markup at 2–3% and refuse to break it out.

- Above $500K monthly, transparent FX terms (e.g., “ECB mid-market + 0.50%”) become achievable.

- Above $5M monthly, multi-currency settlement (settling directly in the cardholder’s currency rather than converting on every transaction) eliminates most of the layer entirely.

The other tactic is to route transactions through local acquirers in the customer’s currency, settling locally and converting in bulk through a treasury provider — which typically prices FX at 10–30 basis points above mid-market rather than 1–3%.

Layer 5 — Ancillaries

The final visible layer on the statement is the bucket of ancillary fees that get little attention individually but add up materially. The main components:

- Chargeback fees. Typically $15–$30 per chargeback, regardless of outcome. A merchant with a 0.5% chargeback ratio on 100K monthly transactions pays $7,500–$15,000/month in chargeback fees alone, separate from the lost transaction value.

- Refund fees. Some PSPs charge $0.30 per refund; others refund the original interchange but keep the acquirer margin; others refund nothing. Read the contract.

- 3DS / authentication fees. $0.03–$0.10 per authentication attempt, including failed and abandoned auths.

- Gateway and monthly fees. Flat $50–$500/month for gateway access, sometimes bundled, sometimes separate. Look for “minimum monthly fees” that quietly kick in below a volume threshold.

- Account update / network token services. $0.05–$0.15 per update, $0.02–$0.05 per network token. These are usually bundled in the headline rate but break out under high-volume usage.

None of these are large individually. In aggregate they typically add 0.10–0.30% to the effective MDR, and on subscription businesses with high refund/chargeback rates, they can add 0.50% or more. They are also the most negotiable layer after the acquirer margin — most PSPs will waive monthly minimums, reduce per-transaction ancillaries, or bundle authentication into the core rate for merchants at scale.

The Sixth Layer — Working Capital

The hidden cost that never appears on the statement is the working capital tied up by rolling reserves and settlement timing.

A rolling reserve holds back a percentage of every transaction — typically 5–10% for low-risk merchants, 15–25% for high-risk verticals like travel, subscriptions, or digital goods — for a window of 90 to 180 days. The funds are released on a rolling basis but never to zero. A merchant processing $500K monthly on a 10% / 90-day rolling reserve has $150K continuously locked up. At an 8% cost of capital, that is $12K/year in unrecoverable financing cost — frequently larger than the chargeback fees, refund fees, and gateway fees combined.

Settlement timing extends the layer. Most PSPs settle T+2 to T+5 (transaction date plus two to five business days), creating an additional float of 1–4% of monthly volume. On $500K monthly, T+3 settlement is roughly $50K of additional working capital tied up at any moment.

The PSP contract red flags briefing covers the specific contract clauses that drive reserve and settlement terms, and which ones are negotiable. For high-volume merchants, the working capital layer is often a larger optimisation target than the visible acquirer margin.

What to Do With This

The MDR stack is not just a teaching frame — it is the decomposition you should be able to do on your own statement before any PSP conversation. The exercise:

- Request an itemised statement. Most PSPs default to blended summaries. Ask for one month, fully itemised, with interchange and scheme fees broken out per scheme.

- Calculate your blended interchange. Sum interchange across all transactions, divide by total volume. Compare against the published Visa and Mastercard interchange tables for your geography and card mix. A wide gap means the PSP’s pass-through is inflated.

- Calculate your blended scheme fees. Same process. Scheme fees should typically run 0.10–0.25% of volume on standard mixes; higher than 0.30% usually means cross-border surcharges, premium-card mix, or PSP markup buried in scheme line items.

- Calculate the residual acquirer margin. Total fees, minus interchange, minus scheme fees, minus measurable ancillaries. The remainder is what your PSP is keeping. Compare against the benchmarks above for your scale.

- Measure FX markup separately. On cross-currency transactions, calculate the spread against mid-market on the same date. If the embedded markup runs above 1.5%, that is the first negotiation lever.

- Quantify the working capital layer. Average reserve balance × cost of capital + settlement float × cost of capital. This is what reserves and timing actually cost you per year.

The operators who win on payments economics are not the ones with the lowest headline rate. They are the ones who can read every layer of the statement, know which layers they can move, and structure contracts that move them. The MDR is not a number. It’s a stack — and every layer has a different owner, a different elasticity, and a different price.

Subscribers get the PSP Selection RFP Kit — 60+ structured questions, evaluation scorecard, and negotiation playbook — delivered to your inbox instantly.