China Payments: The Foreign Operator's Guide

How foreign operators accept Alipay, WeChat Pay, and UnionPay. PBOC licensing realities, CIPS for B2B CNY settlement, and 2024–2026 regulatory changes.

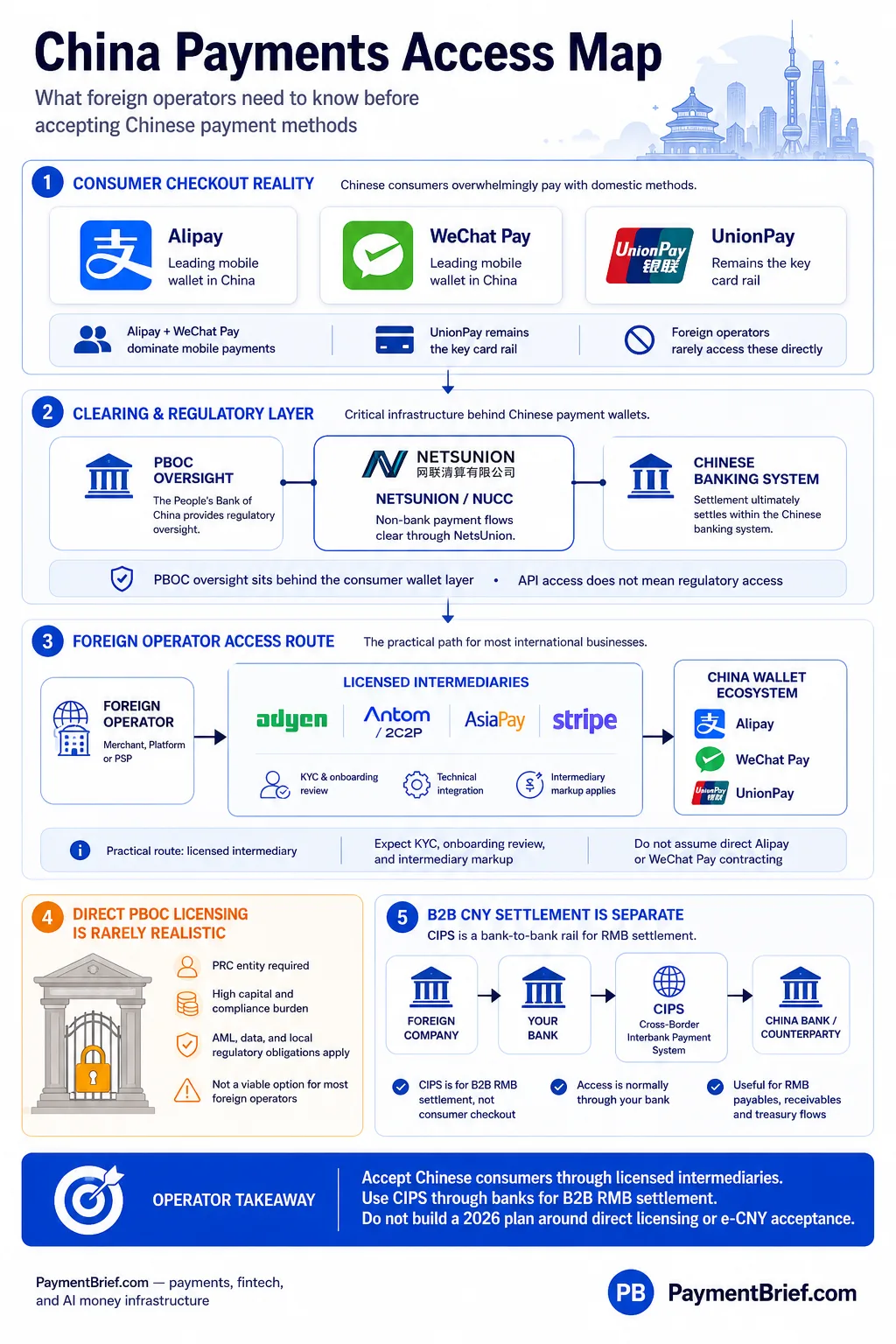

Alipay and WeChat Pay hold over 90% of China's mobile payments, with non-bank clearing routed through NetsUnion. Foreign operators accept them via intermediaries (Adyen, Antom/2C2P, Stripe) — direct PBOC licensing rarely works for foreigners. CIPS handles B2B CNY settlement.

Alipay and WeChat Pay together hold over 90% of China's mobile payments; all non-bank clearing routes through the PBOC-mandated NetsUnion hub. Direct PBOC licensing is rarely a realistic near-term path for most foreign operators — it requires a PRC entity and at least CNY 100 million base capital. In practice, foreign merchants accept Alipay and WeChat Pay through licensed intermediaries such as Adyen, Antom/2C2P, AsiaPay, or Stripe. For B2B CNY settlement, CIPS provides an alternative to SWIFT with 194 direct participants across 126 countries as of April 2026. The e-CNY has reached over 225 million wallets but offers no direct merchant-acceptance path for foreign operators today.

China's payment market is unlike most markets foreign operators encounter. Alipay and WeChat Pay process more mobile payment volume than any card network globally, and the shift from cash to QR-based payments happened in under five years — largely bypassing the card-on-file era that shaped consumer payment habits in Europe and the US. For a foreign operator, this creates a structural challenge: the payment methods your Chinese customers actually use are not accessible the way Visa and Mastercard are. They sit behind a licensing architecture that makes direct merchant agreements effectively unavailable to most foreign entities, and requires routing through a prescribed set of licensed intermediaries.

This guide covers how that system actually works — the duopoly mechanics, the clearing architecture, the realistic paths for foreign operators, and what CIPS means for B2B CNY settlement.

China Payments Access Map — how foreign operators reach Chinese consumers, why direct PBOC licensing is rarely practical, and where CIPS fits for B2B CNY settlement.

The Duopoly: How Alipay and WeChat Pay Work

Alipay (Ant Group) and WeChat Pay (Tencent) together account for over 90% of China's mobile payment market — a duopoly with no close parallel in any other major economy (OECD, Competition in Mobile Payment Services, 2025). Alipay is the larger of the two by most third-party estimates, though the People's Bank of China does not publish a vendor-level market-share breakdown, so the precise split should be treated as a reported estimate rather than an official figure.

Both operate as staged wallets: users pre-load RMB from a linked bank account, and transactions debit the wallet balance. This is distinct from a card-on-file model — the wallet balance mechanism is part of why domestic MDR is structurally lower in China than in most card-dominated markets.

All non-bank payment transaction clearing routes through NetsUnion Clearing Corporation (NUCC) under a PBOC mandate in force since 30 June 2018. Before NetsUnion, Alipay and WeChat Pay maintained direct bilateral connections to individual Chinese banks — giving PBOC limited visibility into transaction flows and allowing both platforms to accumulate financial data outside the central bank's supervision. The mandate ended those direct connections: every non-bank payment now passes through the NetsUnion hub, from which PBOC has full system visibility. For operators, NetsUnion is architecturally invisible (you integrate with Alipay or WeChat Pay at the API layer), but it is the reason the system has the regulatory depth it does.

Under a PBOC draft rule published July 2025, Alipay, Tenpay (WeChat Pay's operating entity), and NetsUnion are being placed under the central bank's direct AML supervision — expanding the directly-supervised entity list from 23 to 27 firms (Caixin Global, July 2025). As a draft measure, the final scope may shift before it takes effect, but the direction is unmistakable: tighter central-bank oversight of the largest payment platforms.

In December 2024, Ant Group restructured Alipay into separate Digital Payment and Alipay Business units — a signal of MDR compression and a pivot toward merchant SaaS and credit services rather than per-transaction fee income. The structural low-cost model that built the duopoly is now a ceiling on growth rather than a competitive weapon.

MDR Rates (Approximate)

Alipay and WeChat Pay domestic merchant fees are typically cited at around 0.55–0.6% by payment-industry sources; PBOC does not publish official MDR schedules and rates vary by merchant category and negotiation. UnionPay card-not-present MDR runs approximately 0.7–0.9% (split roughly between the acquiring bank and UnionPay), and card-present approximately 0.55–0.6%. These are reported approximations — the structural point is what matters: China has among the lowest domestic payment costs of any major market. The constraint is regulatory access, not pricing.

How Foreign Operators Accept Alipay and WeChat Pay

For most foreign entities, there is no realistic direct merchant path. Foreign merchants accept Alipay and WeChat Pay through licensed PSPs and gateways that hold the necessary relationships and infrastructure — not via a direct agreement with Ant Group or Tencent.

Confirmed intermediaries with documented Alipay and WeChat Pay acceptance:

- Adyen — documented support for Alipay, WeChat Pay, and UnionPay across online and POS channels

- Antom / 2C2P — 2C2P is part of Ant International's Antom platform; the Alipay+ / Antom channel is the native route for Ant-ecosystem acceptance globally

- AsiaPay — Hong Kong-headquartered gateway with 17 APAC offices; supports Alipay, WeChat Pay, and UnionPay QR

- Stripe — supports Alipay and WeChat Pay for eligible APAC entities; confirm regional availability for your specific merchant-entity structure

On PingPong: PingPong operates as a cross-border collection, payout, and FX provider for Chinese e-commerce sellers on platforms like Amazon and Tmall Global — not as a checkout-acquiring intermediary for foreign merchants wanting to accept Alipay/WeChat from Chinese consumers. The use cases are different; do not conflate them.

What to expect in practice: Setup typically takes one to four weeks. KYC/AML documentation requirements are non-trivial, and enhanced due diligence on foreign card binding has reportedly tightened through 2025. Total cost is the platform MDR plus the intermediary markup — keep this qualitative unless your provider quotes a specific rate for your merchant category and volume.

Foreign visitor transaction limits (PBOC, March 2024): The single-transaction cap for foreign-card-linked Alipay/WeChat use was raised from US$1,000 to US$5,000; the annual cumulative cap from US$10,000 to US$50,000. Relevant for inbound Chinese tourism acceptance and for testing foreign-linked accounts.

UnionPay: The Third Rail

UnionPay is China's domestic card network — the world's largest by cards issued. All POS terminals in mainland China are legally required to support UnionPay; Visa and Mastercard have very limited domestic acceptance, operating primarily for inbound foreign cardholders. For online merchants targeting Chinese consumers via card payment, UnionPay is the relevant network.

UnionPay International (UPIC) handles foreign-issued UnionPay cards used outside mainland China — a separate entity, relevant for operators serving Chinese travellers or overseas Chinese communities. If you are a foreign merchant outside China looking to capture Chinese tourist spend, UPIC acceptance via your existing acquirer (Adyen, Worldpay, and others have UPIC coverage) is the mechanism.

For foreign operators wanting UnionPay acceptance inside China: route through the same intermediaries as Alipay/WeChat Pay, or via a Chinese acquiring bank — the latter typically requires a PRC entity.

PBOC Licensing: Rarely a Realistic Direct Path

The regulatory framework for non-bank payment institutions was consolidated under the Regulations on the Supervision and Administration of Non-Bank Payment Institutions (released 17 December 2023, effective 1 May 2024). The regulation established two licence categories: (1) Stored Value Account Operation (prepaid wallet issuance and management) and (2) Payment Transaction Processing (merchant acquiring, QR processing, payment facilitation). This replaced a more fragmented prior regime (Han Kun Law, 2024).

Minimum registered capital starts at CNY 100 million under the regulations, with implementing rules specifying higher amounts by business scope. Foreign-controlled entities face additional barriers beyond capital:

- PRC entity required — cannot apply as a foreign company directly; must establish a PRC limited liability or joint stock subsidiary

- Discretionary PBOC approval — approval for foreign ownership is not rule-based; it has historically been rare and slow for entities seeking meaningful operational control

- Ongoing compliance — heightened AML, data-localisation, and PIPL (Personal Information Protection Law) requirements for any licensed entity

For most foreign operators, this makes a direct PBOC payment licence rarely a realistic near-term path. The practical alternatives: partner with or acquire an existing licensed Chinese PSP; operate as a sub-licensee under a licensed entity; or accept that China market access will be intermediated. As of June 2025, there were 169 active Payment Business Licences across all categories — down 37.6% from peak — reflecting the consolidation pressure since the 2021 regulatory tightening.

CIPS for B2B CNY Settlement

CIPS (Cross-Border Interbank Payment System) is China's alternative to SWIFT for RMB cross-border settlement. It is not a consumer payment method — it is interbank infrastructure for CNY flows between financial institutions across borders.

Scale as of April 2026 (CIPS Participants Announcement No. 117):

- 194 direct participants

- 1,597 indirect participants

- 126 countries and regions

- More than 5,100 banking institutions worldwide

The June 2025 expansion added several new direct participants including Standard Bank (South Africa), African Export-Import Bank, First Abu Dhabi Bank, United Overseas Bank (Singapore/Thailand), and Bangkok Bank (Thailand). New CIPS operating rules took effect February 2026.

How CIPS works for operators: Settlement is in RMB only, using a hybrid RTGS and deferred net settlement model. For an operator, CIPS is accessed through your bank — you do not need direct CIPS membership. If your bank participates (directly or indirectly), your RMB cross-border transfers route via CIPS.

Compared to SWIFT for CNY flows: SWIFT still carries most CNY legacy workflows via MT103 and pacs.008 messaging — covered in the SWIFT payment processing guide. CIPS is PBOC's preferred path for China-initiated RMB flows and is faster for banks with direct participation. Both coexist; CIPS is growing in geographic reach and institutional depth.

For operators, CIPS is relevant in three B2B scenarios: a foreign SaaS company billing a Chinese subsidiary in RMB; an exporter receiving CNY payment from a Chinese buyer; a treasury team managing RMB cross-border payables. It is not a consumer checkout infrastructure.

CNAPS, NetsUnion, and Payment Connect

CNAPS (China National Advanced Payment System) is the PBOC interbank backbone, invisible to most operators at the API layer. It runs two main rails: HVPS (High Value Payment System, RTGS for large-value settlement) and IBPS (Internet Banking Payment System, near-real-time retail). Banks use CNAPS to settle with each other; non-bank PSP transactions clear through NetsUnion and then settle against the banking system via CNAPS.

NetsUnion (NUCC) ownership structure includes PBOC and its subsidiaries (~37%), with Alipay, WeChat Pay, and 45 third-party payment companies as members (Caixin Global, 2018 — structure broadly unchanged). The 30 June 2018 mandate requiring all non-bank PSP clearing through NetsUnion is the foundational event for understanding China's current payment architecture. There was no subsequent "full migration" event in 2024 — that date appears to conflate other regulatory milestones; the core migration completed in 2018.

Payment Connect (launched 22 June 2025): A joint PBOC and Hong Kong Monetary Authority initiative linking mainland China's IBPS with Hong Kong's Faster Payment System (FPS) for real-time, cross-boundary retail payments in both RMB and HKD (HKMA press release, 20 June 2025). Six institutions per side participated at launch. This is the first meaningful mainland–HK real-time corridor for small-value retail flows — relevant for operators running HK-entity structures moving funds between Hong Kong and the mainland.

There is no open retail real-time rail in China equivalent to India's UPI or Brazil's Pix. Both UPI and Pix are open to third-party app builders via public APIs. China's real-time infrastructure is exclusively bank/PSP-licensed; no developer-open access layer exists.

e-CNY: Large Scale, Limited Practical Relevance for Foreign Operators

The e-CNY (digital yuan) is PBOC's central bank digital currency and — by cumulative transaction value — the most operationally advanced retail CBDC in the world. Official PBOC data through November 2025 shows approximately 3.48 billion cumulative transactions, a cumulative value of CNY 16.7 trillion, and approximately 225 million personal wallets opened (PBOC, via gov.cn). A framework change effective January 2026 added interest-bearing features, moving e-CNY toward deposit-money characteristics.

For foreign operators, the e-CNY has limited practical relevance today. There is no direct merchant-acceptance path for foreign entities; only licensed banks, major payment platforms, and PBOC-approved operators act as e-CNY intermediaries. Cross-border e-CNY pilots — in Hong Kong, Thailand, and the UAE — are wholesale and B2B, not consumer-facing channels available to foreign merchants. The January 2026 framework change expands domestic utility but does not open a foreign-merchant acceptance route.

This trajectory may shift over a longer horizon. But for 2026 planning purposes, e-CNY is not an acceptance channel foreign operators should build toward.

What This Means for Operators

Accepting payments from Chinese consumers

- Route through a licensed intermediary — Adyen, Antom/2C2P, AsiaPay, or Stripe — for Alipay and WeChat Pay acceptance. No direct merchant agreement path exists for most foreign entities.

- Add UnionPay International coverage if your customers include Chinese travellers or diaspora outside mainland China.

- Budget for platform MDR plus intermediary markup. KYC documentation takes time; start the process early.

- Do not plan around e-CNY acceptance — no direct foreign-merchant path exists today.

For PSPs building China infrastructure

Direct PBOC licensing is rarely a realistic near-term path. More viable routes:

- Acquire or partner with a licensed Chinese PSP.

- Operate as a sub-licensee under a licensed entity.

- Focus on enabling merchant clients to accept Chinese wallets via intermediaries from an offshore position.

For companies with B2B CNY flows

- A CNY bank account at a Chinese bank typically requires a PRC entity. Cross-border CNY transfers use CIPS infrastructure via your bank — no direct CIPS membership is needed.

- Tighten transaction documentation. PBOC and SAFE KYC and record-retention requirements continued to tighten through 2025–2026, and AML and transaction-monitoring obligations on payment institutions and their banking partners are rising.

- Plan for currency controls. CNY is not freely convertible, and cross-border payment and remittance oversight remains strict. Build in lead time for repatriation of material RMB balances and budget for SAFE documentation requirements.

Regulatory watch

- PBOC's July 2025 draft AML rule extending direct supervision to Alipay, Tenpay, and NetsUnion.

- e-CNY framework evolution post-January 2026.

- The ongoing expansion of Payment Connect for mainland–HK real-time flows.

None of these fundamentally change the access constraints for foreign operators in the near term, but they raise the compliance bar for intermediaries — which flows downstream to KYC requirements and onboarding timelines.

Sources & methodology (7)

Alipay and WeChat Pay together account for over 90% of China's mobile payment market — a duopoly with no close parallel in any other major economy

Checked:

Regulations on the Supervision and Administration of Non-Bank Payment Institutions released 17 December 2023, effective 1 May 2024; established two licence categories (Stored Value Account Operation and Payment Transaction Processing); minimum registered capital at least CNY 100 million base

Checked:

CIPS had 194 direct participants, 1,597 indirect participants, and coverage across 126 countries and more than 5,100 banking institutions as of April 2026

Checked:

Official PBOC data through November 2025: approximately 3.48 billion cumulative e-CNY transactions, cumulative value CNY 16.7 trillion, approximately 225 million personal wallets opened

Checked:

Payment Connect — joint PBOC and HKMA initiative linking mainland China's IBPS with Hong Kong's FPS for real-time cross-boundary retail payments — launched 22 June 2025 with six institutions per side

Checked:

PBOC raised the single-transaction cap for foreign-card-linked Alipay/WeChat use from US$1,000 to US$5,000 and the annual cumulative cap from US$10,000 to US$50,000 (March 2024)

Checked:

Under a PBOC draft rule published July 2025, Alipay, Tenpay (WeChat Pay's operating entity), and NetsUnion are being placed under the central bank's direct AML supervision, expanding the directly-supervised list from 23 to 27 firms

Draft rule at time of writing — final scope may shift before enactment

Checked:

Source types explained in our Methodology.